Chilat Doina

July 2, 2026

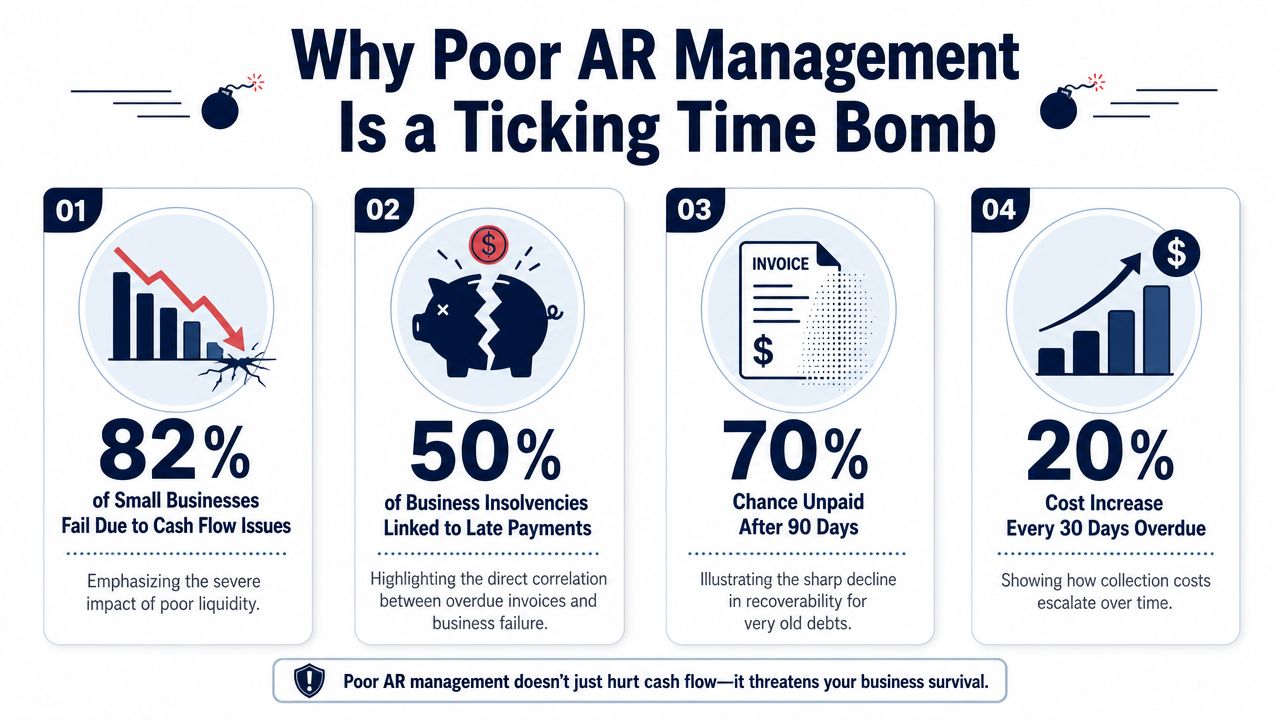

55% of all B2B invoiced sales in the United States are overdue, and in Europe, late customer payments are tied to 25% of business bankruptcies according to Upflow's AR collections statistics. Founders tend to treat accounts receivable as a finance hygiene issue until growth exposes what it really is: a liquidity system.

In e-commerce, that exposure happens fast. You can scale revenue through Shopify, Amazon, wholesale, and marketplaces long before your finance ops are built for complexity. Orders rise, returns rise, channel deductions rise, and what looked like “top-line growth” starts hiding a collections problem, a dispute problem, and eventually a working capital problem.

The brands that stay in control don't run AR like a back-office chore. They run accounts receivable management as an operating discipline that protects cash, preserves customer relationships, and gives leadership cleaner visibility into what revenue is turning into money.

Revenue can grow for months while cash conversion gets weaker. That gap usually shows up first in receivables.

For a high-growth e-commerce brand, AR problems rarely start with one big default. They start with small process failures that stack up across channels. A wholesale invoice goes out two days late because shipping data was incomplete. A strategic account takes an unauthorized deduction and no one resolves it for three weeks. A marketplace reconciliation sits in someone's inbox until month-end. On paper, sales still look healthy. In practice, more working capital stays trapped outside the business.

As noted earlier, overdue B2B invoices are common enough to be a real operating risk, not a finance footnote. That matters even more once a brand adds wholesale, retail, distributors, or larger strategic accounts with payment terms.

The issue is not just slower cash. Weak AR creates noise across forecasting, inventory planning, and customer management. Finance loses confidence in the timing of collections. Operations buys inventory without a clear view of actual liquidity. Sales keeps pushing volume into accounts that may be growing revenue and weakening cash at the same time.

A simple test helps. If your team cannot explain the drivers behind rising receivables without pulling data from multiple systems and rebuilding the story in a spreadsheet, the process will break under more scale.

Poor accounts receivable management usually looks operational before it looks financial:

Many founders err in their understanding of the business. Reported revenue may support the growth story, but delayed collections create pressure on payroll timing, inventory buys, and ad spend flexibility.

That pressure is also avoidable.

Brands that improve your cash flow management usually start by tightening AR execution before looking for outside capital or blunt cost cuts. In many cases, that is the cheaper fix and the cleaner one.

Astute buyers and lenders do not stop at revenue growth. They examine how reliably revenue becomes cash, how disciplined the collections process is, and whether dispute patterns point to larger control issues. A business with drifting aging, frequent deductions, and inconsistent follow-up will look less predictable, even if demand is strong.

For e-commerce brands, there is another trade-off. Aggressive collections can protect near-term cash and still damage customer lifetime value if the approach is tone-deaf. A customer-centric AR model solves for both. It sets clear terms, fast escalation paths, and tighter internal controls, but it also separates strategic accounts, legitimate disputes, and at-risk customers from simple delinquency. That is how brands protect liquidity without burning repeat business.

If you want a clean benchmark for how fast receivables are converting, start with Days Sales Outstanding and how to interpret it. The metric matters because valuation follows consistency. Cash that arrives on time is worth more than revenue that needs constant chasing.

Strong AR makes the business easier to trust.

Most founders track revenue, contribution margin, and ad spend with real precision. Then they manage receivables with a monthly aging export and gut feel. That gap is expensive.

If you want tighter control, build a small AR dashboard and review it with the same discipline you use for inventory and marketing. You don't need dozens of metrics. You need a handful that tell you whether sales are converting to cash on time and where friction is building.

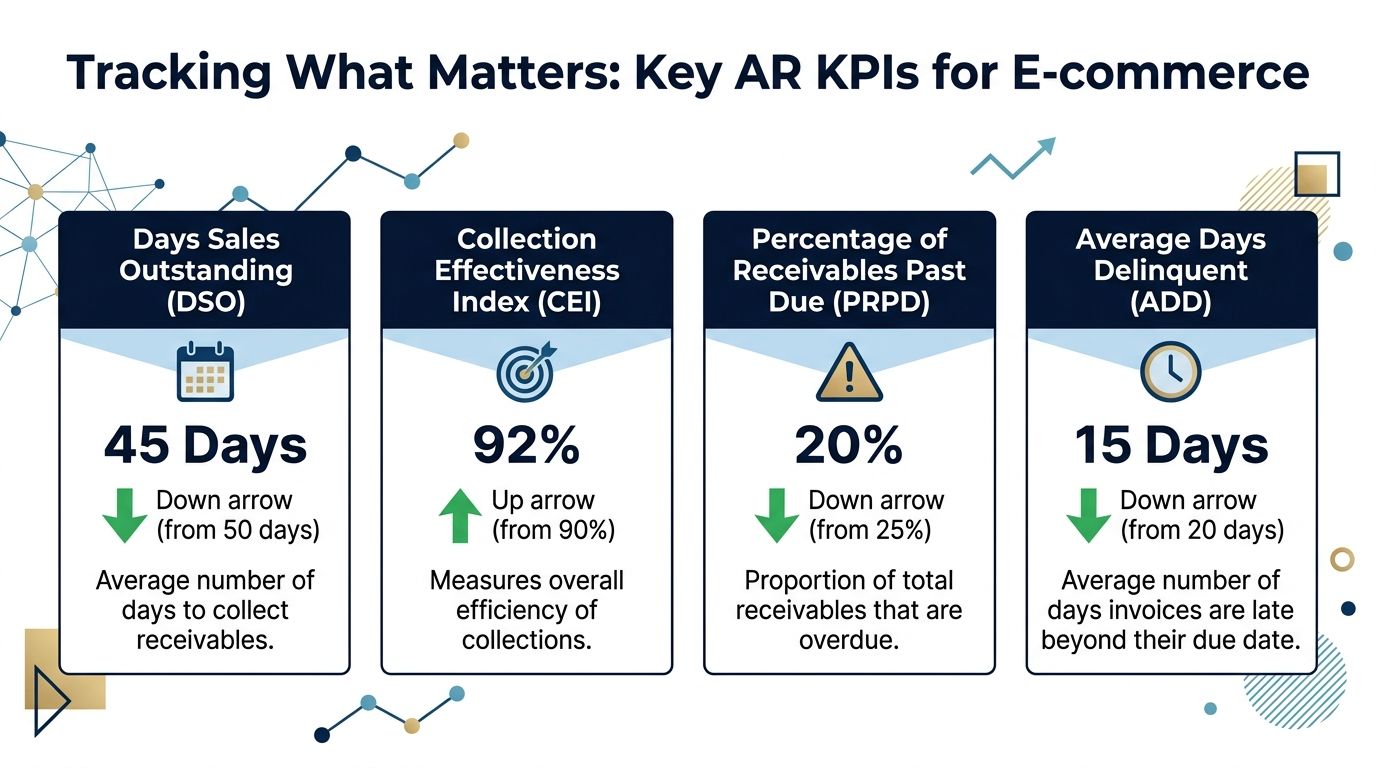

The core benchmark is Days Sales Outstanding, or DSO. The formula is (Accounts Receivable ÷ Total Credit Sales) × Number of Days in Period, as outlined in Esker's breakdown of AR benchmarking metrics. That same source notes that finance leaders are prioritizing a 10% quarterly reduction in DSO in 2026 as a liquidity goal.

Lower DSO means your company is turning credit sales into cash faster. Higher DSO means more working capital is stuck outside the business.

For an e-commerce founder, DSO matters most when you sell through channels that don't pay instantly. Wholesale, retail partners, enterprise gifting, and marketplace claims all push you into receivables exposure. If DSO creeps up, your growth may be consuming cash faster than you realize.

If you need a plain-English refresher on the metric itself, this Days Sales Outstanding explainer is worth bookmarking.

DSO is the headline metric, but it's not enough on its own. I'd track AR with a mix of efficiency, aging, and quality signals.

| KPI | What it tells you | How to use it |

|---|---|---|

| DSO | Average time to collect after a credit sale | Watch trend direction, not just one period |

| AR Turnover Ratio | How often receivables are collected over a period | Useful for spotting slowing collection velocity |

| CEI | How effectively the team collects available receivables | Good for measuring execution quality |

| Average Days Delinquent | How late invoices are beyond agreed terms | Helps isolate delinquency from standard terms |

| Percentage Past Due | Share of receivables already overdue | Highlights aging stress quickly |

The AR Turnover Ratio measures how often receivables are collected in a year, while CEI helps you judge collection effectiveness rather than just elapsed time. Those two are especially useful when channel mix changes. A DSO move may reflect more wholesale exposure. A CEI decline usually points to execution slippage.

Don't let one aggregate number hide channel-specific problems. Marketplace deductions, wholesale invoices, and enterprise gifting receivables behave differently and should be reviewed separately.

A useful AR dashboard drives action:

If you're building the basics, this accounts receivable guide for startups can help frame turnover analysis and the early reporting discipline founders often skip.

The point isn't to admire KPIs. It's to make late cash visible early enough to fix it.

A lot of AR policies fail because they're written like legal documents and enforced like panic responses. Neither works well in e-commerce.

If your brand depends on repeat buyers, channel reputation, and long-term account value, collections can't default to punishment. The better model is structured, consistent, and customer-aware. That doesn't mean soft in the sense of passive. It means deliberate about when to push, how to push, and which accounts deserve flexibility.

For major e-commerce brands, overly aggressive AR tactics can increase churn by up to 15%, according to JPMorgan's receivables insights. That's the statistic most founders miss. A collections win that damages retention isn't always a win.

This matters even more for brands with high repeat purchase behavior. If a valuable customer hits a billing issue, duplicate charge concern, return timing mismatch, or account confusion, a harsh collections motion can turn a solvable service issue into a lost relationship.

The best collections policies create consistency first, then nuance. I'd structure it around customer segments and predefined actions.

Not every overdue balance should be handled the same way.

That segmentation matters because collections is part finance, part customer experience. A premium brand shouldn't send the same sequence to a loyal wholesale partner that it sends to a risky new account.

Protect cash without making good customers feel like bad actors.

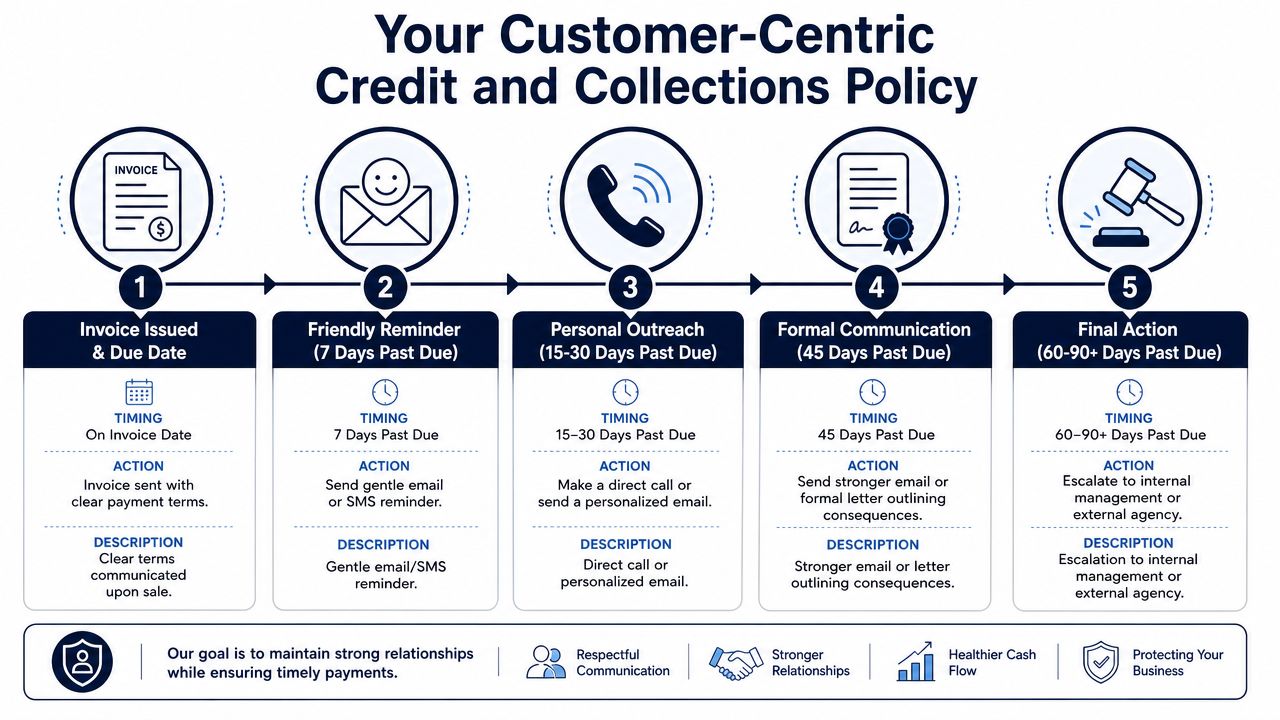

A customer-centric cadence still needs deadlines. Here's the version that tends to work in real operations:

At invoice issuance

Make terms impossible to miss. Include due date, payment methods, PO references, and support contact details.

Shortly before due date

Send a friendly reminder. Keep it operational, not confrontational.

When payment becomes overdue

Shift from automated reminder to human review. Check for missing documents, receiving issues, returns, or billing disputes before escalating tone.

If the balance continues aging

Move to direct outreach from finance. Be specific about the invoice, prior communication, and required action.

If the issue remains unresolved

Escalate internally before outsourcing pressure. Sales, account management, and operations may be able to unblock what finance alone can't.

Your written policy should answer the questions teams otherwise improvise:

The policy should also define what not to do. Don't threaten penalties your team won't enforce. Don't let sales override finance without documented approval. Don't bury disputes in inboxes.

A good collections policy reduces improvisation. A great one does that while preserving customer lifetime value.

Accounts receivable breaks down when teams treat it as a single event. It isn't. It's a chain.

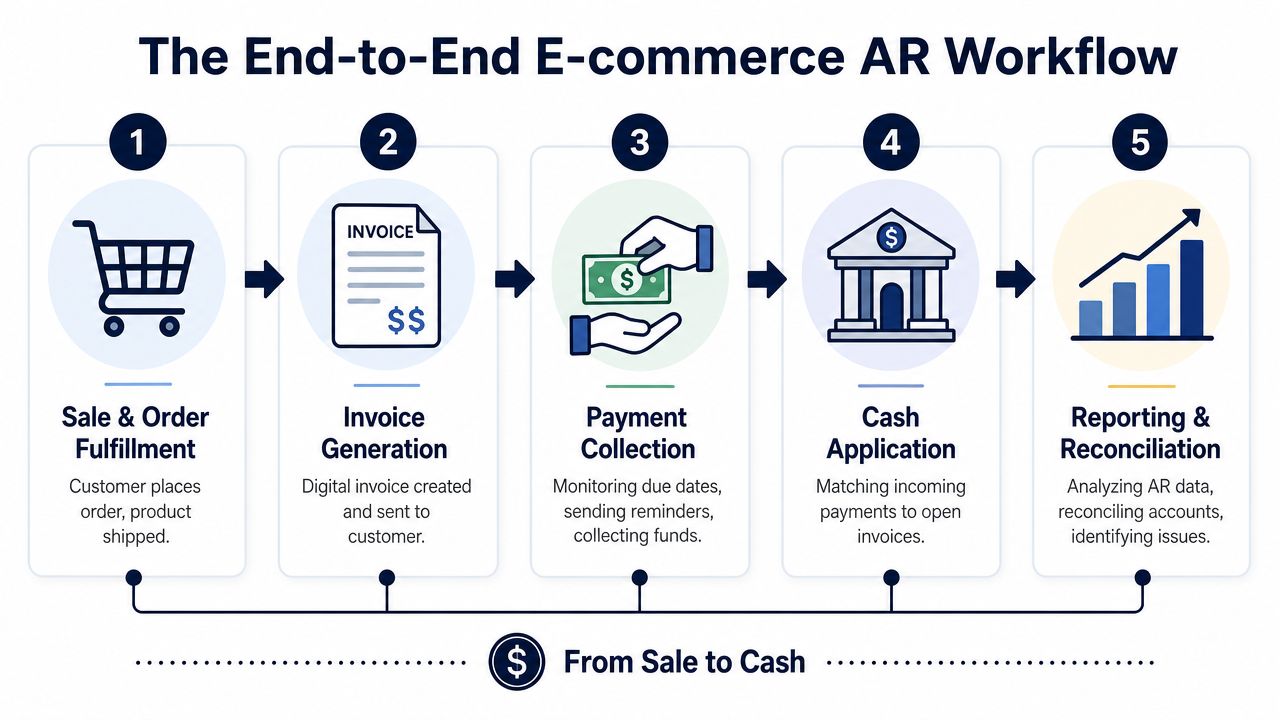

A payment delay that surfaces in finance often starts upstream in fulfillment, customer service, returns, or channel operations. That's why founders need to see the whole workflow, not just the aging report. The sale, invoice, payment, dispute, and reconciliation steps all affect each other.

AR starts when a customer order creates a financial obligation. In e-commerce, that can happen through Shopify, Amazon, a wholesale PO, a distributor portal, or an ERP-created sales order. If the order data is incomplete at that stage, every downstream process gets harder.

For example, a wholesale shipment might leave the warehouse on time, but if the billing entity, PO number, tax treatment, or delivery confirmation is wrong, the invoice becomes contestable. Finance sees a late balance. Operations caused it days earlier.

The order is placed, inventory is allocated, and the product ships. Channel-specific rules then enter the picture. Marketplace orders behave differently from direct invoices. Wholesale and retail accounts often need more documentation attached to the order trail.

The invoice should be generated promptly and accurately. That means matching line items, discounts, shipping, taxes, references, and terms to what the customer expects. Most avoidable disputes begin here.

Once the invoice is live, collection begins before the due date. Good teams monitor open balances, scheduled reminders, and account-level exceptions. Weak teams wait until something is visibly overdue.

If collections starts only after an invoice ages, you've already given away time.

This step gets less attention than it deserves. Money can hit the bank and still not clear the operational issue if your team can't match payment to the right invoice, deduction, or return. Unapplied cash creates false aging, messy books, and bad decision-making.

Reconciliation is the process by which the system's effectiveness is proven. It should surface unapplied payments, disputed balances, duplicate invoices, short-pays, and recurring issue patterns by channel or customer.

Most AR friction happens in handoffs, not in one team's technical skills.

The fix is operational ownership. Every exception should have one home, one owner, and one system of record. If your team is solving the same issue in Slack, email, and spreadsheets, the workflow isn't a workflow. It's a series of workarounds.

Founders don't need to memorize every accounting step. They do need to ensure the order-to-cash chain is clean enough that revenue can move through it without friction.

Manual AR works right up until it doesn't. A founder or controller can hold the system together for a while with spreadsheets, inbox follow-ups, and tribal knowledge. Then volume rises, channel complexity multiplies, and the cracks show all at once.

That's the point where automation stops being a “nice to have” and becomes infrastructure.

Companies using dedicated AR software report a 30% faster cash conversion cycle and a 50% reduction in write-offs, and 91% of mid-sized firms with fully automated AR systems report increased savings and improved cash flow according to HighRadius on accounts receivable management. Those aren't cosmetic improvements. They change how much cash the business can retain and redeploy.

The strongest argument for automation isn't labor savings alone. It's control.

A good AR stack helps with several things at once:

The bigger your channel sprawl, the more important integration becomes. If your data sits separately in Shopify, Amazon reports, your ERP, your returns platform, and your bank feed, you don't have one AR process. You have several partial ones.

A scalable setup needs more than invoice reminders. It should fit your operating model.

I'd prioritize clean integration with tools your team already depends on, especially systems like Shopify, NetSuite, and the rest of your commerce operations stack. If you're evaluating broader finance tooling around your store operations, this review of best accounting software for ecommerce can help frame where AR should sit within the larger system.

Customers pay faster when it's easy to understand what they owe and how to resolve issues. That means portals, accessible statements, clear remittance workflows, and straightforward dispute submission.

Any software can process the clean cases. The ultimate test is what happens when there's a short-pay, duplicate payment, missing PO, return offset, or channel deduction.

For teams thinking through digital outreach and repayment convenience, Intelligent Contacts' collections automation is a useful example of how self-service and automation can support collections without making the customer experience worse.

A short overview helps illustrate how modern AR tools fit into the finance stack:

Some habits look lean but create hidden cost:

That model may save software spend in the short run. It usually burns far more in delayed cash, write-offs, and management distraction.

A fast-growing seller can post strong top-line growth and still miss payroll timing, delay inventory buys, or lean too hard on debt because receivables are tied up in deductions, returns, and unresolved claims. At 8 figures, that gap usually comes from complexity, not from a lack of invoicing discipline.

AR starts behaving less like a collections queue and more like an operating signal. Wholesale terms, marketplace reimbursements, retailer chargebacks, return offsets, and customer-specific dispute patterns all convert to cash on different timelines. If finance treats them as one pooled balance, the forecast gets noisy and management reacts late.

Revenue is a starting point. Cash planning gets more accurate when AR is segmented by how each balance clears.

In practice, that means forecasting by channel, customer type, and exception pattern. A clean wholesale invoice with signed proof of delivery should not sit in the same forecast bucket as a marketplace claim under review or a retail account that regularly nets deductions against open invoices. Those balances carry different timing, different risk, and different staffing needs.

A forecasting model for this stage usually includes:

The goal is not precision to the dollar. The goal is a forecast that reflects how cash moves through the business. That is the foundation of better working capital planning and optimization.

High-growth commerce brands often misclassify return-related balances as standard collections work. That creates delay because the issue is usually not willingness to pay. It is broken reconciliation between the order, the return event, the warehouse decision, the refund, and the deduction taken downstream.

That distinction matters if customer lifetime value matters. A customer-centric AR model does not waive valid charges to keep the peace, and it does not default to aggressive outreach when the underlying issue is still unresolved. It separates true credit risk from service friction, then routes each case to the team that can fix it fastest.

Classify disputes at intake

Separate credit issues, return-related deductions, pricing disputes, and documentation gaps as soon as they enter the queue. Different causes need different owners.

Match every deduction to a source event

Tie the balance to the order, return authorization, warehouse receipt, carrier scan, refund record, and any marketplace ruling.

Set clear legitimacy rules

Define what counts as an approved offset, an invalid denial, an operational error, or a recoverable charge.

Route cases beyond finance

Many aging items are created by returns operations, fulfillment, customer support, or channel compliance. Finance should own the visibility, not every fix.

Track repeat root causes

If the same channel, SKU family, warehouse node, or returns policy keeps creating leakage, that issue belongs on the operating agenda.

At scale, write-offs often come from fatigue. Teams get tired of chasing unclear balances, the file ages, and someone clears it just to close the month.

The stronger approach is to reduce the time between exception intake, owner assignment, documentation review, and resolution. Shorter cycles improve cash flow, but they also protect good customer relationships. Customers with legitimate questions get faster answers. Chronic abusers get identified earlier. Finance gets a cleaner view of what is collectible, what is operational noise, and what should change in policy.

That is how mature AR teams protect both cash conversion and CLV.

Brands usually think of AR as a defensive function. Collect what's owed. Reduce overdue balances. Keep the books clean. All of that matters, but it's too narrow.

Handled well, accounts receivable management improves much more than collections. It strengthens working capital, surfaces weak operational handoffs, protects customer relationships, and gives leadership a more honest view of how the business converts sales into usable cash.

When a brand builds disciplined AR systems, several things happen at once:

That last point gets underestimated. Discerning investors and buyers don't just value growth. They value control. A company that collects well, reconciles cleanly, and resolves disputes quickly presents lower operational risk.

The strongest founders stop asking, “How do we chase invoices faster?” and start asking, “How do we design a revenue-to-cash system that scales?”

That shift changes the work. AR policy becomes part of customer strategy. Workflow design becomes part of finance strategy. Automation becomes part of valuation strategy. If you're serious about building that bigger discipline, working through broader working capital optimization is the right lens.

Strong AR isn't about being stricter. It's about being clearer, faster, and harder to break as the business grows.

A customer-centric model is what makes this sustainable for e-commerce. You still protect cash. You still enforce terms. But you do it without blindly harming the relationships that drive repeat revenue and brand value.

That's the playbook worth building. Not because AR is exciting. Because cash control is.

If you're operating at scale and want sharper operator-to-operator insight on systems like this, Million Dollar Sellers is where serious e-commerce founders compare what's working across Amazon, DTC, and omnichannel brands.

Join the Ecom Entrepreneur Community for Vetted 7-9 Figure Ecommerce Founders

Learn MoreYou may also like:

Learn more about our special events!

Check Events