Chilat Doina

July 10, 2026

Revenue is up. Your ad account is spending more every month. Inventory purchase orders are larger than they used to be. On paper, the business looks stronger than ever, yet cash feels tighter, decisions feel slower, and every surprise hits harder than it should.

That's the seven-figure plateau most e-commerce founders eventually run into. The operating system that got you here stops working once you're managing larger inventory bets, channel-level profitability, international sales, and a business that could become a real wealth event. At that point, advanced financial planning stops being an accounting function and becomes a leadership function.

Most founders don't need another budget template. They need a financial cockpit that shows what's happening, what breaks under pressure, and where capital should go next.

A fast-growing brand can still hit a cash wall.

That usually happens when sales momentum outruns financial discipline. The founder knows the top line, the media buyer knows blended ROAS, the operator knows lead times, and the bookkeeper closes the month after the fact. Nobody owns the full picture in real time.

That gap gets expensive once your inventory cycle expands and your downside scenarios get sharper. A large PO placed at the wrong time, a return-heavy product line, or a temporary ad cost spike can turn a profitable quarter into a liquidity problem. The issue usually isn't lack of effort. It's lack of integrated planning.

The discipline that changes this is advanced financial planning built around operating decisions, not just accounting outputs.

At lower revenue levels, founders can get away with reviewing the P&L once a month and managing cash from the bank balance. At higher levels, that approach becomes reactive. You're no longer just running a store. You're allocating capital across inventory, customer acquisition, team growth, taxes, and future personal wealth.

The labor market reflects how much more valuable this capability has become. In the United States, employment of personal financial advisors is projected to grow 10 percent from 2024 to 2034, with about 24,100 openings on average each year, and the median annual wage reached $102,140 in May 2024, according to the U.S. Bureau of Labor Statistics profile on personal financial advisors. Founders should read that as a signal. Financial sophistication is increasingly a competitive advantage.

Practical rule: If your financials only tell you what happened last month, you're already late.

Great operators often assume more sales will solve most problems. In e-commerce, more sales can amplify weak planning. More volume means more cash trapped in inventory, more exposure to returns, and more complexity across tax and entity decisions.

The founders who break through don't just sell more. They build systems that let them see risk early, protect liquidity, and turn profits into durable wealth.

A founder approves a bigger inventory buy for Q3, pushes spend into Meta to support the launch, and feels good because the top-line plan still says the year is on track. Six weeks later, returns come in above plan, CAC rises, a supplier slips production, and the forecast turns out to be a revenue target with no operating logic behind it.

That is the difference between a spreadsheet and a forecast model.

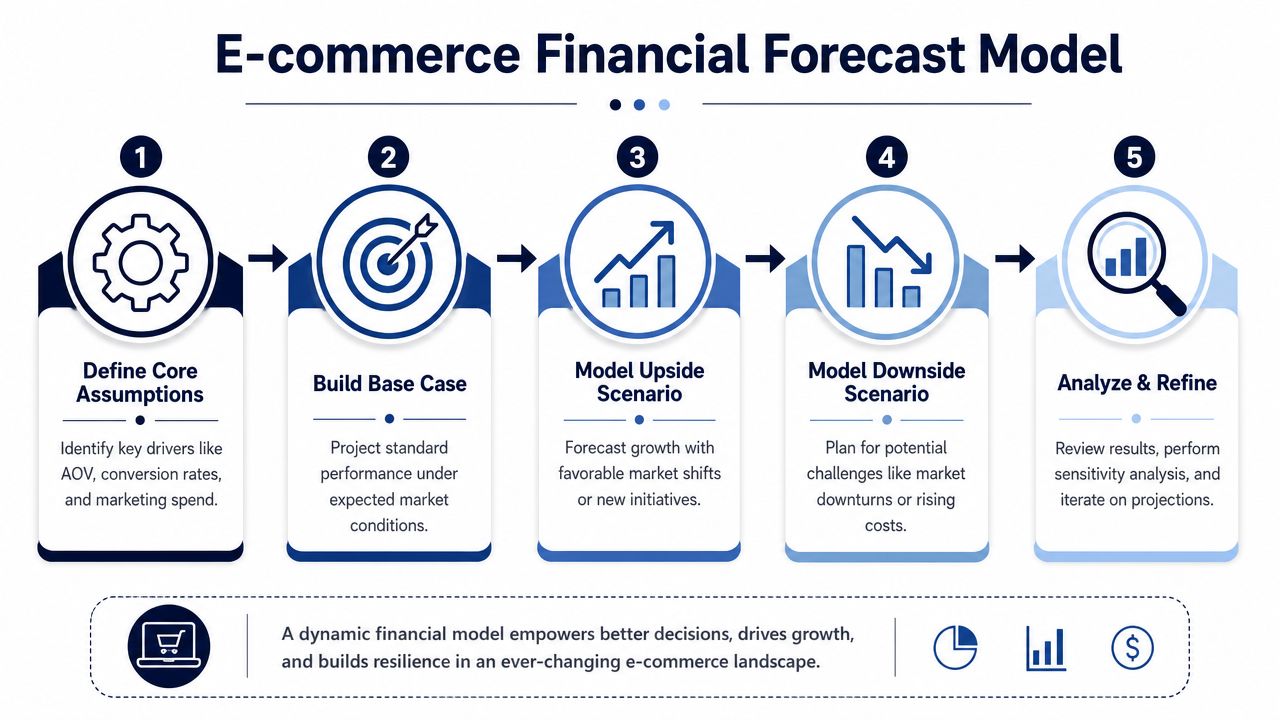

At 7 to 9 figures, forecasting starts below revenue. The model needs to show what creates demand, what reduces net sales, and what survives after fulfillment, discounts, channel fees, and returns. For most brands, the core inputs are traffic, conversion rate, average order value, discount rate, return rate, product mix, contribution margin, and channel-level customer acquisition efficiency.

Segmentation matters more than founders want it to. A blended model hides the truth. Amazon can make the business look healthier than DTC. Wholesale can inflate revenue while compressing cash generation. International expansion can raise sales while creating VAT, duty, transfer pricing, and repatriation issues that never show up in a simple growth assumption.

Build the model so each channel stands on its own economics.

A practical structure looks like this:

That last step is where advanced planning starts to look different. Founders building toward a multi-million dollar exit need a model that does more than budget the income statement. Buyers care about earnings quality, working capital discipline, and whether growth is consuming cash faster than it creates value.

A single-case model usually reflects what the founder wants to happen. A useful model reflects what the business can absorb.

Use three scenarios. Base case, upside case, downside case. Keep them grounded in actual operating conditions, not mood. The base case assumes the current plan executes with normal seasonality and current channel economics. The upside case should come from a specific event, such as a launch that lifts repeat purchase rate or a supply chain improvement that expands in-stock depth on best sellers. The downside case should be uncomfortable and plausible, such as rising CAC, weaker conversion during promo periods, delayed inventory receipts, tariff pressure, or a returns spike in one category.

Good scenarios answer questions management can act on:

That is what separates financial planning from annual budgeting. The model becomes a decision tool.

The forecast does not need to predict the quarter perfectly. It needs to show where the business breaks and what you will do when it does.

Revenue forecasting is the easy part. Margin forecasting is where weak models fall apart.

Category mix changes everything. One product line can carry strong AOV and low return rates, while another drives volume but destroys contribution after freight, discounts, and customer support. Founders who only watch blended gross margin usually find the problem after they have already scaled the wrong demand.

Track margin by category, channel, and customer cohort where possible. Then pressure-test the assumptions behind it. If paid traffic shifts toward lower-intent audiences, conversion may dip while return rates rise. If Amazon share grows, fee drag can offset the volume gain. If international expansion accelerates, margin may tighten before scale benefits show up.

For founders who need cleaner inputs before building a forecast, this guide to financial statement analysis helps tighten the reporting layer the model depends on.

I have seen founders overbuild these models into something only finance can touch. That is a mistake. A strong forecast should be detailed enough to catch risk early and simple enough that finance, ops, supply chain, and growth can review it in one meeting and know which assumptions changed.

Use a model you can update fast. Review assumptions monthly. Rework scenarios when a major variable shifts. Tie each line to an owner.

If nobody owns the assumptions, the forecast turns into decoration.

You place a seven-figure PO in August, freight slips, Amazon pays on its cycle, Meta spend stays high, and your P&L still looks fine. Then payroll, VAT, and the supplier balance hit in the same two-week window. That is how a profitable e-commerce brand gets forced into bad decisions.

At 7 to 9 figures, liquidity breaks on timing, not on whether the business is profitable in theory. Annual budgets smooth over the exact weeks when cash gets tight. Monthly reporting arrives after the problem has already shown up.

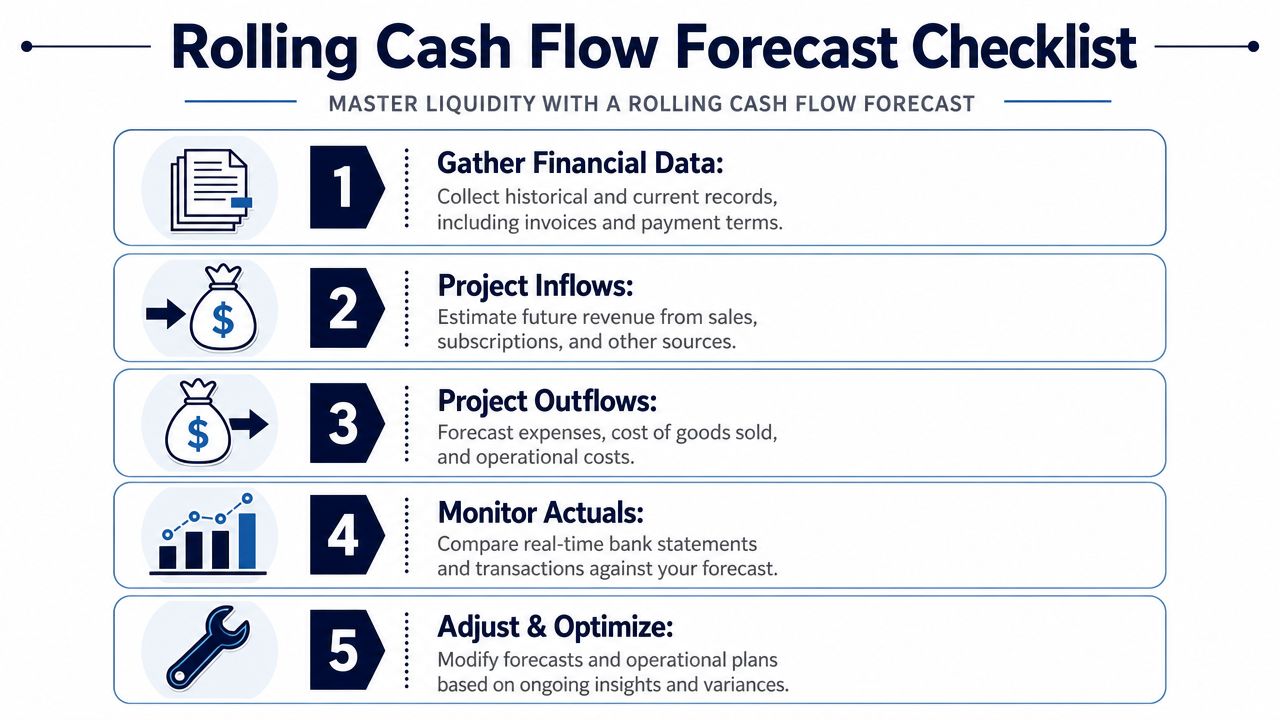

A 13-week rolling cash flow forecast fixes that by forcing weekly visibility into collections, inventory commitments, ad spend, tax payments, debt service, and distributions. I have found this is the shortest cadence that still gives management enough time to act. You can push a PO, trim paid spend, speed up collections, or draw on a facility before the bank balance gets ugly.

It also creates discipline across functions. Finance owns the model, but ops, supply chain, growth, and the founder all have inputs that change the cash outcome.

Keep it built on actual cash movement, not accrual logic.

That means expected inflows from Shopify, Amazon, wholesale receivables, subscriptions, and financing proceeds. Then map the outflows in the order cash leaves the business: supplier deposits, production balances, freight, duties, 3PL fees, payroll, software, agencies, rent, debt payments, tax installments, and owner distributions.

For larger brands, I prefer adding three operating layers that basic models miss:

The model should also show beginning cash, ending cash, undrawn credit, and a minimum cash threshold. If the forecast breaches that threshold, the response should already be assigned.

Founders usually blame finance after the squeeze shows up. The source is often purchasing.

The common pattern is simple. Demand looks strong, the team commits to more inventory, and the forecast treats that inventory like a balance sheet asset instead of a series of cash exits. In e-commerce, especially with overseas manufacturing and international expansion, cash can leave 90 to 150 days before the related revenue is fully collected. Add FX swings, duty payments, and slower wholesale terms, and liquidity tightens fast.

Black Friday is the obvious version of this problem, but not the only one. New market launches, large retailer orders, and tariff changes can create the same strain. A founder planning for a multi-million dollar exit cannot afford to run the business quarter to quarter with cash surprises. Buyers discount companies that look operationally strong but require constant working capital triage.

If you want a tighter operating system around inventory, payables, receivables, and cash conversion, this guide on working capital management for growing businesses is worth reviewing.

A weekly cash review should end with decisions, not commentary.

Use it to reset PO timing based on sell-through and weeks of cover. Reallocate paid media toward channels with faster cash payback. Pull forward collections from wholesale accounts before a heavy inventory week. Rework payment terms with suppliers before you need the concession. If a gap is coming, arrange financing early, while performance still gives you options.

I also track a downside case every week. Not a theoretical disaster scenario. A realistic version where returns run high, one shipment lands late, and paid efficiency softens. That habit matters more once the business has multiple entities, cross-border tax exposure, or a planned exit timeline, because a short-term cash mistake can create expensive tax and deal consequences later. For founders thinking about owner distributions and broader tax planning for small businesses, liquidity planning should sit in the same decision loop.

The brands that stay in control are not always the fastest growers. They are the ones that know, week by week, what cash will be demanded and which lever to pull before pressure turns into damage.

The structure you started with often stops being the structure you should keep.

A founder can build a strong brand inside the wrong tax or legal setup and not feel the pain until profits rise, distributions grow, or international sales create exposure in places they weren't watching.

The right structure depends on what you're building toward.

If you want pass-through treatment, simpler owner economics, and efficient current distributions, one structure may fit better. If you want to retain earnings, raise outside capital, issue equity cleanly, or create a more conventional acquisition wrapper, another may fit better. The mistake is choosing once and treating that choice as permanent.

A useful lens is to ask four questions:

The answers shape more than taxes. They affect governance, investor readiness, and the quality of your eventual exit.

Cross-border sales add complexity faster than most founders expect. Nexus, VAT, transfer pricing considerations, foreign subsidiaries, marketplace collection rules, and local filing obligations can all show up before the finance function is ready for them.

Recent data shows 57% of U.S. ecommerce sellers now generate over 30% of revenue internationally, yet only 12% of financial planning resources provide actionable guidance on cross-border tax optimization, according to Fidelity's advanced planning commentary for ultra-high-net-worth planning. That gap matters because founders can create double taxation and compliance issues by scaling into new markets without redesigning the structure around them.

For a practical overview of tax planning for small businesses, this resource from EndureGo Tax is a useful reference point before you bring in specialist advice.

A solid review should cover where revenue is sourced, where inventory sits, where contracts are signed, where IP is held, and where intercompany relationships may need to be formalized.

Here's a helpful primer to pair with that process:

Founders often think they'll “clean this up later.” Later is expensive.

Restructuring under pressure, especially during diligence or after expansion, tends to create unnecessary friction. Tax planning works best when it's tied to operating reality early. If you're reviewing distributions, intercompany flows, and owner compensation only after the accountant closes the year, you're not planning. You're documenting.

For founders tightening this area, this guide to tax optimization strategies is a strong internal reference.

Once the business starts generating real cash, your main job changes.

You're no longer just deciding how to grow revenue. You're deciding where capital earns its highest strategic return. That may be inside the brand. It may be outside the brand. It may be in a structure that protects personal wealth from operating risk.

Most founders default to reinvesting because growth feels productive. Sometimes that's right. Sometimes it's a habit that hides weak discipline.

Every excess dollar generally belongs in one of three places.

First, you can reinvest in the core business. That includes inventory depth, new products, better talent, creative output, retention systems, and selective paid growth. This works best when the business still has clear, repeatable opportunities with strong unit economics.

Second, you can extract profit and diversify. That protects you from having all your net worth tied to one operating asset. Founders who never do this often discover they built a valuable business but fragile personal balance sheet.

Third, you can buy adjacent assets. That may mean acquiring smaller brands, complementary distribution, or assets that strengthen your current moat. Acquisition can be powerful, but it also multiplies integration risk and management load.

Capital allocation is where founder maturity shows up. Anyone can spend money. Fewer people can rank opportunity cost correctly.

Reinvestment only makes sense when the return profile is better than your alternatives after risk, complexity, and time are considered.

That means you should pressure-test each use of cash against questions like these:

Advanced financial planning gets personal. Some founders should be more aggressive inside the business. Others should be taking more chips off the table.

Financial planning has shifted toward digital and technology-driven solutions, with big data analytics enabling hyper-personalized financial strategies, and there's also a growing emphasis on ESG investments, according to Finance Strategists' overview of financial planning trends. For founders, the practical takeaway isn't trend-chasing. It's that better tooling can improve decision quality both inside and outside the business.

Inside the company, analytics can sharpen customer segmentation, forecast margin by cohort, and improve inventory planning. Outside the company, more advanced planning tools can help match distributions and investments to personal goals, liquidity needs, and risk tolerance.

What works is intentional diversification tied to a clear founder thesis.

What doesn't work is oscillating between starving the business and overfunding it because the bank balance happens to be high that month.

If you want optionality later, you need to build for sale long before a buyer appears.

Many e-commerce founders think exit planning starts when they hire a broker. It starts much earlier, in the way the business reports financials, documents processes, structures contracts, and reduces dependence on the founder.

Buyers don't just buy growth. They buy confidence.

That confidence comes from clean financial statements, clear SKU economics, stable contribution margins, documented operating processes, supplier relationships that survive owner transition, and revenue that isn't dangerously concentrated. A messy but profitable business can still trade below its potential because the buyer prices in uncertainty.

Twelve to twenty-four months before a potential sale, founders should tighten the basics:

A sale price is only part of the outcome. The after-tax result matters more.

Asset Map notes that advanced financial planning for high-net-worth e-commerce founders often misses the connection between business succession and multi-generational wealth transfer, even though 43% of founders plan to exit within the next 5 years, and that gap can erode 25 to 30% of net proceeds through tax inefficiencies, according to its discussion of financial planning for high-net-worth individuals. That's the hidden leak in many exits. Founders optimize for valuation, then give away too much of the outcome because the ownership and estate structure weren't built ahead of time.

Exit lens: Don't ask only, “What is the company worth?” Ask, “What do I keep, what happens next, and who controls the asset before and after closing?”

The cleanest exits are usually the result of compounding preparation.

A useful way to understand this:

| Phase | What matters most |

|---|---|

| Early build | Product-market fit, repeatable growth, margin discipline |

| Scale phase | Professional reporting, channel diversification, process documentation |

| Pre-exit window | Earnings quality, legal cleanup, team depth, diligence readiness |

| Deal process | Negotiation leverage, tax structure, transition plan |

| Post-close | Liquidity management, wealth transfer, reinvestment strategy |

Founders who treat exit planning as ongoing operating discipline usually get two advantages. They create a better business now, and they preserve more options later. Even if you never sell, building a company that could be sold improves how the company runs.

Monday morning. Ads spent hard over the weekend, Amazon is holding reserves, one 3PL invoice landed early, and the merchandising team wants to place a large PO before your best seller slips out of stock. If your reporting stack cannot show cash impact, margin impact, and payback timing in one view, the business is running on instinct.

At 7 to 9 figures, control comes from operating rhythm, not more reports. The founder, finance lead, operator, and channel owners need one scorecard, one meeting cadence, and clear rules for what happens when a metric breaks range. Otherwise every team defends its own numbers and nobody owns the financial outcome.

A useful dashboard is narrow. It answers the questions that change spend, purchasing, pricing, and working capital decisions this week.

Top-line revenue, sessions, and blended MER have their place. They do not explain where cash is being created or consumed. The better view goes deeper. Which SKUs still hold margin after returns and fulfillment? Which channel looks efficient on platform reporting but weak after discounting and payment fees? Which cohort is worth reacquiring at current CAC, and which one should be left alone?

For advanced operators, the KPI stack usually includes:

I like a simple rule here. A channel should earn the right to scale. If LTV to CAC is below your threshold after returns, discounting, and support cost, cut spend, fix the economics, or accept that it is a brand channel and stop calling it profitable. Many operators use 3:1 as a baseline. The exact threshold depends on gross margin, repayment cycle, and how much inventory that growth forces you to carry.

| KPI | What It Measures | Target Benchmark |

|---|---|---|

| Gross Margin by SKU | Profitability after direct product costs at the item level | Review monthly by product category |

| Contribution Margin Post Ad Spend | Profit left after variable selling and marketing costs | Protect margin floors before scaling spend |

| Inventory Turnover | How efficiently inventory converts into sales | Monitor with days-on-hand metrics |

| 13-Week Cash Position | Near-term liquidity and cash risk | Review weekly |

| LTV:CAC by Channel | Customer acquisition efficiency by source | Set a minimum threshold and enforce it by channel |

| Profit Extraction Target | Whether growth is creating owner liquidity | Set explicitly and review regularly |

Governance matters just as much as the dashboard.

The metric stack works when meetings follow a fixed cadence and every KPI has an owner. The founder should not be the catch-all escalation point for every variance. The head of growth owns channel payback. Operations owns inventory health and landed margin assumptions. Finance owns cash visibility, forecast variance, and the rules behind spend approval. That structure matters more once you sell across borders, hold inventory in multiple jurisdictions, or run a mix of DTC, marketplace, and wholesale revenue. One loose definition of margin can create expensive mistakes in tax, transfer pricing, and capital planning.

A practical governance rhythm looks like this:

The goal is simple. No surprises, no vanity reporting, and no growth decision without a clear view of margin, cash, and payback. That is the difference between a founder who runs a bigger store and one who controls a valuable financial asset.

At a certain scale, the founder's edge isn't just product instinct or media buying. It's capital judgment.

That means seeing the business as both an operating company and a financial asset. It means modeling downside before it arrives, protecting liquidity before it gets tight, structuring tax and ownership with the end in mind, and treating every retained dollar like it has competing jobs to do.

That's the key shift in advanced financial planning. You stop running only for revenue. You start building for resilience, optionality, and long-term wealth.

The brands that separate from the pack usually don't have fewer problems. They have better financial control, better decision timing, and a clearer framework for what to do next.

If you're a serious operator who wants to compare notes with founders already navigating these decisions at scale, Million Dollar Sellers is where many of the best 7, 8, and 9-figure e-commerce entrepreneurs trade real playbooks, pressure-test ideas, and scale smarter.

Join the Ecom Entrepreneur Community for Vetted 7-9 Figure Ecommerce Founders

Learn MoreYou may also like:

Learn more about our special events!

Check Events