Chilat Doina

June 3, 2026

You're probably in one of three spots right now.

A supplier wants a bigger inventory commitment than your current cash position can support. Your paid media team is telling you there's room to push harder, but you know ad platforms collect their money before blended margin shows up in your bank account. Or a smaller brand is available at a price that makes strategic sense, and the only thing standing between you and the deal is liquidity.

That's where most conversations about business loan options go sideways. Founders start shopping for “the lowest rate” as if every dollar of debt is interchangeable. It isn't. The right facility for a large inventory buy is often the wrong one for ad spend. The right structure for an acquisition can create breathing room. The wrong one can trap a growing brand in weekly payments that choke cash flow.

Cheap money isn't always the best money. Fast money isn't always bad money. The question is whether the structure matches the job.

A lot of founders treat borrowing like a rescue move. In e-commerce, that's usually the wrong frame. Used well, debt is a timing tool. It lets you buy inventory before the season hits, fund customer acquisition while contribution margin is still attractive, or move on an opportunity before a competitor does.

Founders love headline APR. Lenders know that. But a lower advertised cost doesn't help much if the process is too slow for your purchase order window, your inventory lands after peak demand, or the facility comes with restrictions that limit how you can deploy capital.

There's a more useful split: accessible capital versus affordable capital.

According to NerdWallet's overview of women-owned business financing, online lenders are often easier to qualify for but can carry higher effective rates, while microloans are often capped at $50,000. That matters because “easy approval” often means you're paying for speed, flexibility, or looser underwriting in some other way.

Practical rule: If a lender asks for less proof, expect to pay for that convenience somewhere in the structure.

A simple way to think about business loan options is this:

Most debt problems in e-commerce don't come from borrowing. They come from borrowing the wrong kind of money for the wrong reason. If you finance a long-payback initiative with short-term expensive debt, your business starts serving the lender instead of the growth plan.

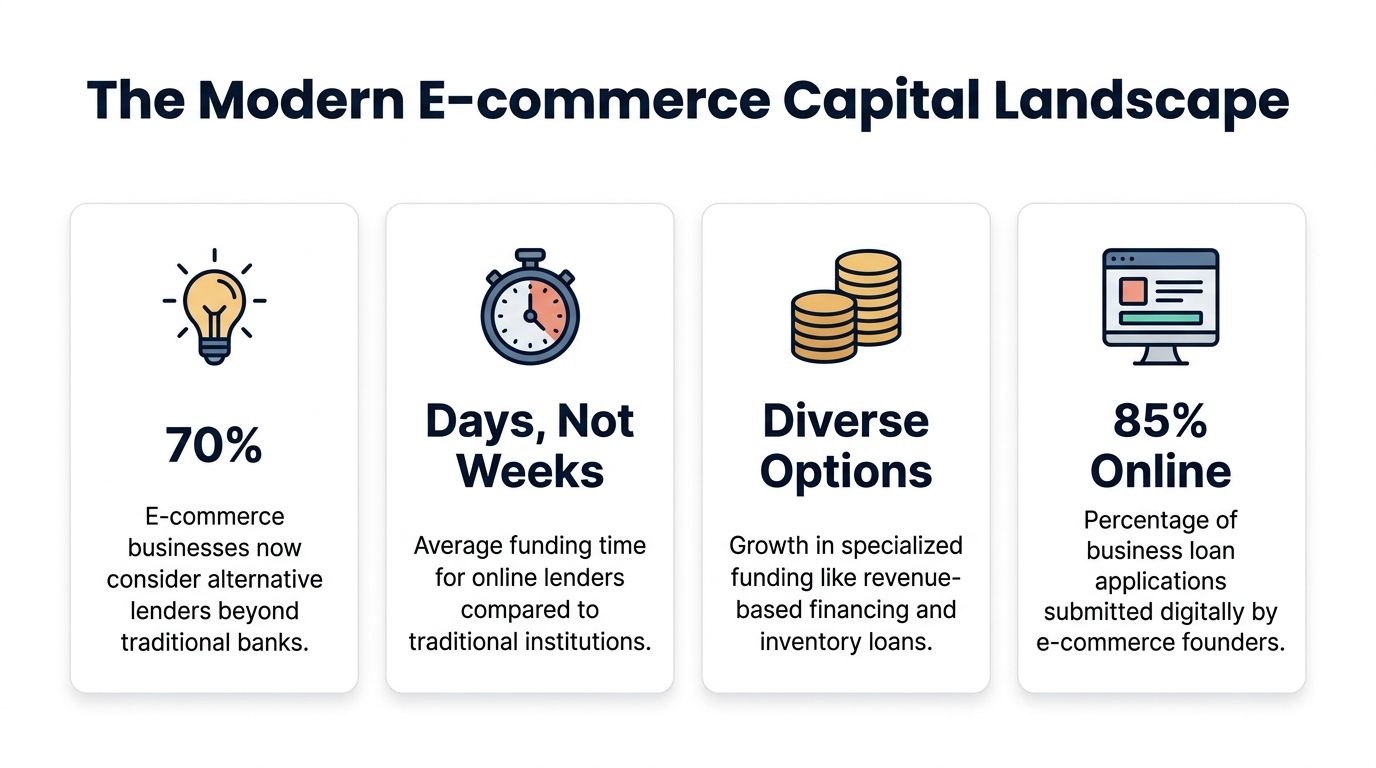

The old playbook was simple. You went to your bank, brought tax returns, and hoped the relationship manager cared enough to push your file through. That world still exists, but it's no longer the whole market.

The U.S. small-business credit market is estimated at $1.4 trillion, according to the Bipartisan Policy Center's explainer on the small-business financing market. The same analysis notes that outstanding small-business loans at depository institutions rose from $173 billion in 1995 to $368 billion in 2019, finance companies held nearly $400 billion in small-business credit, and online lenders held about $25 billion in 2019.

That shift matters because e-commerce brands don't all fit one underwriting box. A bank may like your profitability but hate your inventory concentration. A fintech lender may understand marketplace cash flow better but charge more for the risk. A finance company may be more comfortable with asset-backed structures than a traditional branch lender.

You're not choosing between “bank loan or no bank loan” anymore. You're choosing among lenders that optimize for different things:

That's why generic advice fails. The best lender for a mature omnichannel brand with stable wholesale receivables may be the wrong fit for an Amazon-heavy seller with aggressive inventory turns.

If you want a broader look at channels outside traditional lending, this guide on funding for ecommerce business is a useful complement to the debt-focused view here.

More options sounds good until you realize each option prices risk differently. That's why founders need a filtering framework, not a bigger list.

The labels matter less than the use case. What matters is how the capital behaves once it hits your account.

A term loan is best for a defined project with a clear payback logic. Think warehouse racking, equipment, expansion into a new channel, or a one-time inventory move where you want predictability.

You get a lump sum and repay it on a fixed schedule. That makes term debt easier to model. It also makes mistakes more expensive, because the payment clock starts whether the initiative works or not.

Good fit: larger one-time uses of capital with a reasonable forecast.

Bad fit: experimental ad spend or volatile short-cycle needs.

A line of credit is the operator's tool. You draw when needed, repay, and draw again. For e-commerce, that's useful when Meta spend ramps faster than expected, a supplier wants an early deposit, or cash collections arrive later than purchase commitments.

A line of credit is less about increasing returns through debt and more about smoothing timing mismatches. It works best when the business is healthy but cash conversion isn't perfectly smooth.

Good fit: working capital, ad spend buffers, temporary inventory gaps.

Bad fit: large strategic projects that need long runway.

An SBA 7(a) loan sits closer to long-duration business financing. It's often a fit when the capital need is meaningful and the use is broad enough to justify a structured underwriting process.

For a scaled brand, that could mean refinancing expensive debt, funding working capital with a longer horizon, or supporting an acquisition where monthly payment pressure needs to stay manageable.

This isn't speed capital. It's planning capital.

A CAPLine is more specialized. For seasonal e-commerce businesses, that matters. If your cash gets tied up in inventory and receivables ahead of a recurring sales spike, a revolving structure can make more sense than a standard term loan.

This kind of facility is about rhythm. You use it because your business expands and contracts in a pattern the lender can understand.

If you're buying a specific physical asset, equipment financing can make sense because the asset itself often anchors the structure. For brands operating their own warehouse, light manufacturing, or fulfillment systems, this can be cleaner than using a general-purpose loan.

The main advantage is alignment. The thing you buy is the thing being financed.

Revenue-based financing works when you want capital tied more directly to future sales than fixed amortization. In practice, founders often use it when they believe the growth opportunity is real but don't want a rigid monthly payment structure.

The upside is flexibility relative to standard debt. The downside is cost transparency can get murky fast if you don't model the full repayment outcome carefully.

This is one of the business loan options that gets overused by brands chasing growth without a clear margin map.

This is emergency or highly tactical money. It can solve a short-term problem, but it can also create a larger one if you use it to fund something with uncertain payoff.

If your gross margin is already under pressure, high-frequency repayment structures can turn a decent business into a permanently cash-starved one.

Microloans and community-based programs can be useful for smaller capital needs, especially for newer businesses. But for a 7- or 8-figure seller, they're usually too limited to solve a serious inventory or growth financing challenge.

If you operate internationally or have entities outside the U.S., country-specific financing rules matter more than generic advice. For example, founders exploring how to secure working capital in UAE should look at local underwriting norms, trade finance realities, and how lenders treat cross-border revenue.

Founders usually ask the wrong question first. They ask, “What loan can I get?” The better question is, “What exactly am I financing, and how fast does that investment pay back?”

That's the filter that keeps you from using a blunt instrument for a precise job.

If the use of funds is inventory for a known seasonal ramp, you want flexibility and a structure that matches a recurring cash conversion pattern. If the need is longer-term working capital or a strategic project, you want a longer runway and lower monthly pressure. If the use is ad spend, you need to be honest about volatility. Ad platforms can turn efficient spend into dead spend fast.

The SBA makes this distinction clearly. A Seasonal CAPLine and 7(a) loan comparison from the SBA shows that a Seasonal CAPLine is designed to finance cyclical increases in receivables, inventory, and sometimes labor costs, while 7(a) loans can go up to $5 million with terms up to 25 years for real estate or 10 years for equipment, working capital, or inventory. In plain English, short-cycle volatility fits revolving credit better. Longer-lived investments fit amortizing debt better.

| Funding Type | Best For | Typical Cost | Speed | Key Consideration |

|---|---|---|---|---|

| Term loan | One-time expansion project, warehouse buildout, major inventory buy | Usually structured as interest-bearing debt with scheduled repayment | Moderate to slow | Best when payback is clear and timing is not urgent |

| Line of credit | Cash flow gaps, ad spend swings, supplier deposits | Often higher than the cheapest bank debt but flexible | Moderate to fast | Useful buffer, but easy to misuse for permanent needs |

| SBA 7(a) | Long-term working capital, refinancing, acquisition support | Often more affordable than convenience lending | Slower | Documentation burden is heavier |

| SBA CAPLine | Seasonal inventory and receivables cycles | Structured around revolving working capital use | Slower than fintech options | Best if seasonality is predictable and documented |

| Equipment financing | Warehouse or operating equipment | Asset-linked cost structure | Moderate | Strong fit only when tied to a specific equipment purchase |

| Revenue-based financing | Growth initiatives tied closely to sales flow | Can become expensive depending on structure | Fast | Model total repayment, not just convenience |

| Merchant cash advance | Short-term urgent liquidity | Frequently the most expensive path | Very fast | Can damage cash flow if margin is thin |

Use this lens before you apply:

For founders weighing debt against dilution, this piece on equity financing vs debt financing is worth reading alongside your lender conversations.

And if your business is earlier in its lifecycle or still evaluating where debt fits versus equity, this overview of the startup funding process for founders helps frame when each capital source tends to make sense.

Don't finance experimentation with debt that assumes certainty. That mismatch is where expensive mistakes happen.

What works is simple. Use debt when the return path is visible, the repayment schedule matches the operating cycle, and the facility leaves room for normal volatility.

What usually doesn't work is using fast, high-cost debt to cover structural problems. If your inventory planning is weak, contribution margin is unstable, or ad performance swings wildly, borrowing can amplify the weakness instead of solving it.

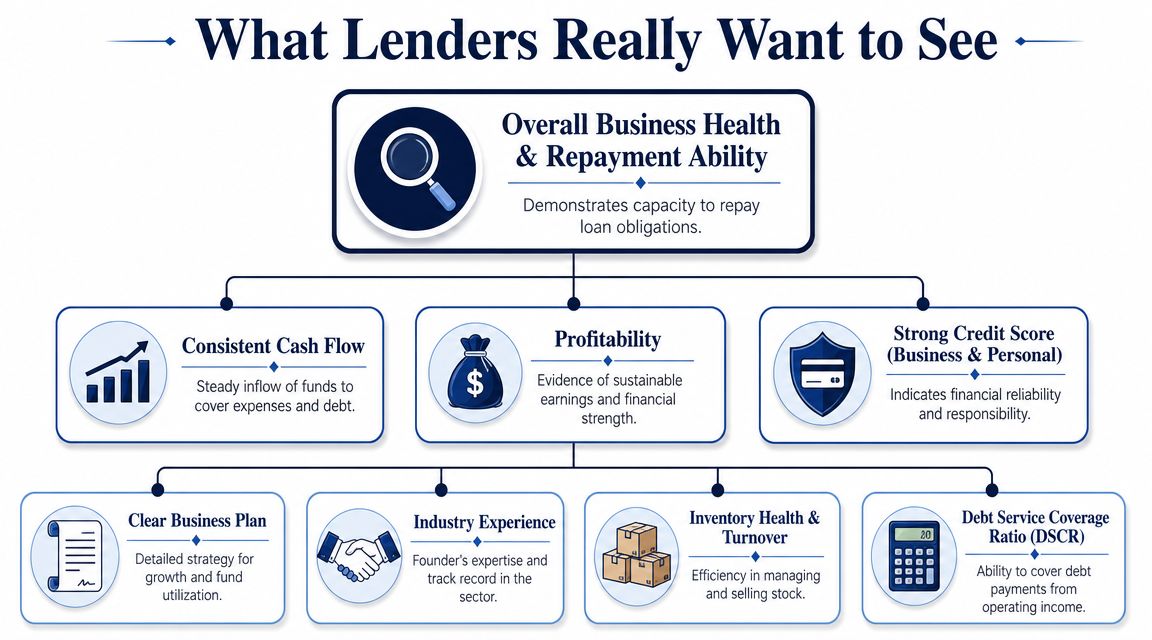

Most founders think lenders start with revenue. Serious lenders start with repayment.

Two brands can post similar annual sales and get very different credit decisions. The reason is usually hidden in the monthly detail. One business has steady collections, manageable inventory commitments, and controlled debt. The other has lumpy cash flow, margin swings, and too much dependence on one channel or one hero SKU.

Lenders care about whether the business can absorb a bad month without breaking the repayment plan.

A useful benchmark is Debt Service Coverage Ratio, or DSCR. According to First Southern Bank's guidance on business loan approval requirements, lenders commonly look for a minimum 1.25 DSCR, meaning the business generates $1.25 of cash flow for every $1.00 of scheduled debt service. Stronger files often show 1.35–1.50+, which gives lenders more comfort on both approval and pricing.

They don't just ask whether sales are growing. They ask whether the business is durable enough to make payments during stress.

Here's what they typically examine:

A lender doesn't need your business to be perfect. They need to believe it stays solvent when a few things go wrong at once.

Before you ask for money, look at your business the way underwriting will.

If cash management is still too reactive, fix that before you apply. This guide on how to manage cash flow is a practical place to tighten the operating side before you hand your numbers to a lender.

A sloppy application tells the lender you run a sloppy business. That may sound harsh, but it's true. Approval isn't only about financial strength. It's also about how easy you make it for the underwriter to understand your company.

The process is competitive. Lendio's loan statistics and trends summary reports that only 59% of SBA loan applications in 2023 received some form of approval, with 34% fully approved and 25% partially approved. The same source says 85% of owners see speed to approval as important when choosing a lender. Clean preparation helps on both fronts.

Here, stronger operators separate themselves.

A short explainer can also help if your model looks unusual on paper. For example, if one SKU family drives most of your volume, explain the product cycle, reorder cadence, and why concentration risk is manageable.

This walkthrough is worth watching if you want a plain-English primer before organizing the full package:

The fastest approvals usually go to founders who answer the next underwriting question before it gets asked.

The best founders don't think about debt as a necessary evil. They think about it as a controlled financial tool.

Used badly, debt creates pressure, weakens decision-making, and forces short-term moves. Used well, it lets you buy deeper when others can't, stay in stock during critical windows, smooth cash conversion, and act on strategic opportunities without giving up ownership.

That's the main point of comparing business loan options. You're not shopping for money. You're choosing a structure that supports a specific move.

Start with the business objective. Then choose the financing tool. Then pressure-test the repayment path.

If the capital supports a proven inventory cycle, a predictable working capital pattern, or a well-understood expansion, debt can be a serious advantage. If the capital is covering poor planning or wishful forecasting, the same debt becomes expensive noise.

Founders outside the U.S. should also remember that underwriting standards vary a lot by market. If you need a region-specific reference point, this guide to the requirements for securing business finance shows how lenders often evaluate the borrower profile and documentation side in another jurisdiction.

The brands that win don't just raise capital. They deploy it with precision.

If you want sharper operator-to-operator insight on financing decisions, inventory strategy, and what's working inside high-growth brands, Million Dollar Sellers connects you with experienced e-commerce founders who are already navigating these choices at scale.

Join the Ecom Entrepreneur Community for Vetted 7-9 Figure Ecommerce Founders

Learn MoreYou may also like:

Learn more about our special events!

Check Events