Chilat Doina

May 5, 2026

You’re probably in one of two spots right now.

Either the business is still growing, but you can feel the weight of founder dependence, channel concentration, and messy financials that would get exposed the second a serious buyer starts digging. Or the business is mature enough to sell, but you don’t know whether you’re sitting on a clean, premium asset or just a decent cash-flowing operation that will trade at an ordinary multiple.

That distinction matters.

A strong ecommerce exit rarely comes from “putting the business up for sale” and hoping the market rewards the effort you’ve already put in. Good exits come from shaping the company into something a buyer can underwrite with confidence. Premium exits come from reducing risk, proving transferability, and creating enough strategic logic that more than one buyer wants the deal.

If you want to learn how to sell ecommerce business the right way, think less like an operator trying to cash out and more like a founder packaging an asset for institutional scrutiny. The work starts long before the LOI.

A founder gets an inbound offer after a strong quarter, feels the rush, and assumes the hard part is done. Then the buyer starts asking better questions. How dependent is growth on one paid channel? Who runs operations day to day? Are supplier terms documented and transferable? Can the numbers survive a quality-of-earnings review? That is where valuation expands or gets cut.

Preparing for a sale is not cosmetic work. It is asset engineering.

Buyers paying premium multiples are not buying a Shopify storefront with recent growth. They are buying earnings they believe will hold after the founder is gone, plus a structure that lets them own the upside without inheriting hidden risk. That means the prep work is less about polishing the pitch and more about reducing uncertainty in the places that affect price, holdbacks, earnouts, and retrade risk.

Founders with meaningful revenue often focus too much on growth rate and too little on transferability. Serious acquirers look at both. A business with stable margins, clear controls, documented processes, and buyer-ready reporting often gets better terms than a faster-growing business that still depends on founder instinct. As discussed by Frictionless Commerce on selling angles and acquisition value, acquirers assign more value to assets that are hard to copy and easy to inherit.

A premium exit starts with defensibility.

If the business relies on one supplier relationship in your DMs, one media buyer who has never documented a testing process, or one founder who approves every decision, the buyer sees fragility. They may still proceed, but they will protect themselves through a lower multiple, a larger earnout, or tighter reps and warranties.

The strongest ecommerce businesses usually have a few traits in common:

The point is simple. Buyers pay more for earnings that look durable and portable.

Founders usually pitch upside. Buyers investigate failure points.

That work falls into three areas: financial control, operational transfer, and concentration risk. Each one affects valuation. Each one also affects deal structure, which matters just as much as headline price.

Messy books do more than slow diligence. They create doubt about every other claim in the deal.

Get the accounting cleaned up well before you go to market. Buyers want monthly financials they can follow without needing the founder to translate them. They want expense categories that make sense, inventory accounting that ties out, and add-backs that are documented rather than argued. If margins move, there should be a clear reason. If cash flow differs from reported profit, be ready to explain working capital, inventory timing, and any unusual one-off events.

Good financial preparation usually includes:

I have seen small accounting fixes create outsized valuation gains because buyers price off earnings, and every dollar of credible profit gets multiplied.

Many otherwise solid businesses, at this point, become disadvantaged.

A buyer wants to know the company can function on Monday morning without the founder improvising the answer to every problem. That requires process ownership, role clarity, system access control, and backup coverage for key functions. If one employee, one freelancer, or one founder account sits at the center of everything, the buyer sees a handoff problem.

Prepare for that scrutiny with a practical checklist:

If you want a stronger planning framework before sale prep starts, review this guide to business exit strategy planning for founders.

Concentration is manageable until a buyer models what happens if the concentrated asset weakens.

One paid channel driving customer acquisition is a risk. One major SKU carrying most of the profit is a risk. One supplier with no formal agreement is a risk. Founder-led creative, founder-led partnerships, and founder-led brand trust can also become valuation pressure points if the buyer believes performance drops after handoff.

The answer is not to eliminate every concentration issue before a sale. That is rarely realistic. The answer is to show control, mitigation, and a credible path to continuity. If one channel dominates, prove that CAC discipline, contribution margin, and retention support the model. If one supplier matters disproportionately, formalize terms and broaden relationship coverage. If the founder is still the face of the brand, build assets the team can operate without you.

A strong exit narrative explains why the business has worked, why the earnings should continue, and where a new owner can improve performance without rewriting the whole company.

That story needs proof. Margin expansion from better merchandising. Retention gains from product improvements. Lower return rates from operational fixes. Better forecasting discipline. More stable inventory turns. Acquirers reward upside when the current engine already works.

If you want outside perspective on whether the business is ready for market, Lighthouse Consultants' business sale expertise is a useful benchmark for the kind of sale-readiness work that improves both valuation and deal terms before outreach starts.

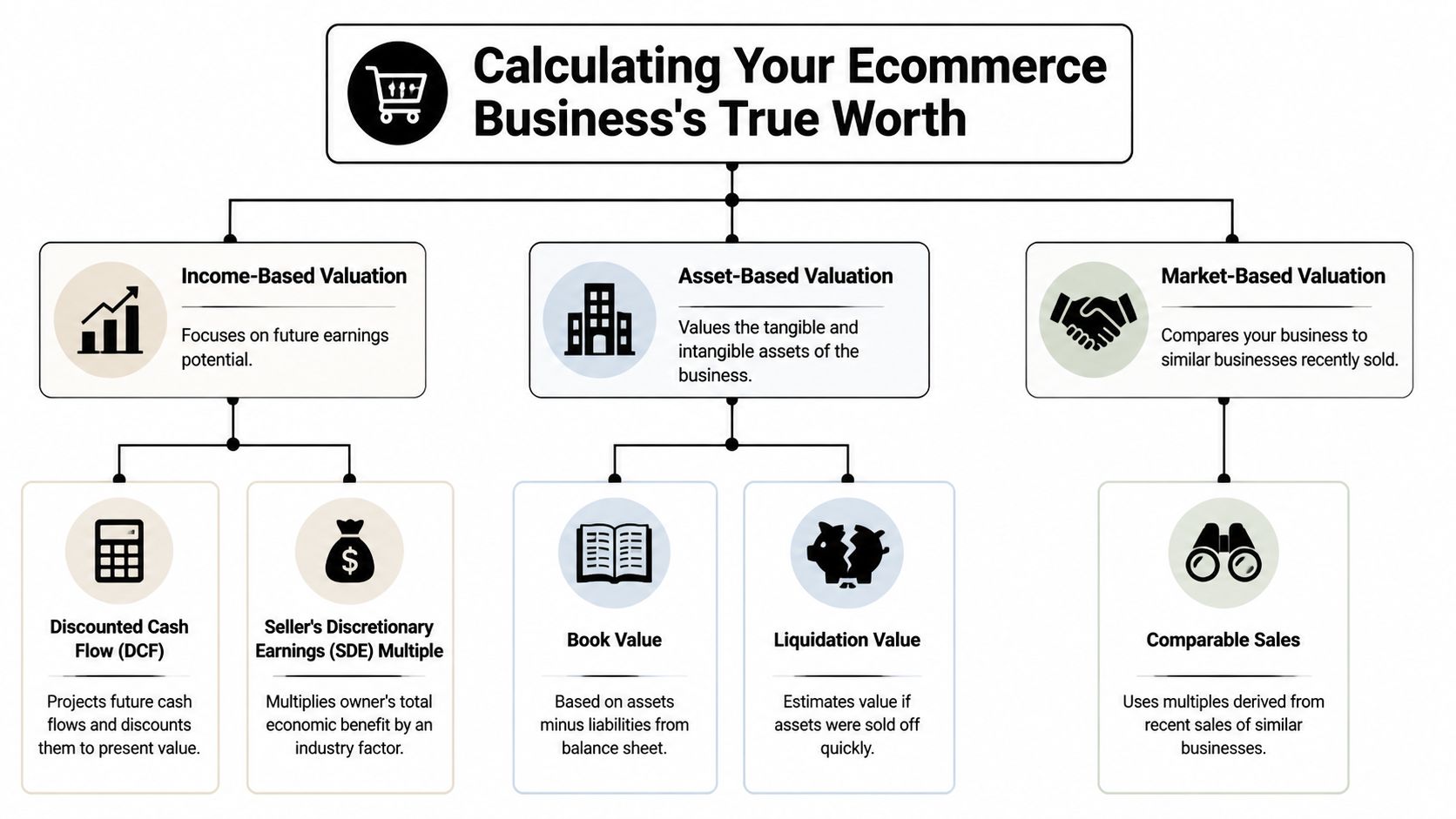

A founder gets an LOI at a number that feels life-changing, then diligence starts and the price drops because the earnings were overstated, the add-backs were weak, or the buyer priced in more risk than the seller expected. That gap usually starts long before the offer. It starts with a loose view of value.

For an owner-operated ecommerce business, valuation usually begins with Seller’s Discretionary Earnings, or SDE. Buyers use SDE to answer a practical question: what cash flow does this business produce for a new owner after stripping out expenses that will not continue? Start with profit, then adjust for owner compensation, personal expenses run through the company, and one-time costs that are documented and non-recurring.

The quality of the valuation depends on the quality of the normalization. A buyer will not pay for “adjusted profit” unless the adjustments are clean, consistent, and easy to verify in the general ledger, bank statements, payroll records, and tax returns.

A useful SDE normalization usually separates:

I push founders to be conservative here. Aggressive add-backs do more than reduce credibility. They invite a buyer to re-underwrite the whole P&L.

Practical rule: If an add-back cannot be supported with documents and explained in one sentence, do not assume you will get paid for it.

Once SDE is clean, the essential work begins. The multiple decides whether you have an average exit or a premium one.

Buyers do not pay the same multiple for two businesses with the same profit if one has durable repeat purchase behavior, stable margins, channel discipline, clean reporting, and a team that can run the operation after handoff. They discount the business with concentration, uneven contribution margin, poor forecasting, or founder dependence because they expect earnings to degrade after close.

That is the core valuation mechanic. Buyers are pricing future confidence in the cash flow, not congratulating past revenue growth.

For a closer benchmark on how acquirers underwrite this, review how to value an ecommerce business for sale. The framework is useful because it forces the right question: how much of this earnings stream is durable, transferable, and defensible?

SDE is the working language for many ecommerce deals, but it is not the only lens that matters. Strong founders know when another framework changes the conversation.

Asset-based logic matters more if inventory, proprietary formulations, trademarks, or other hard assets carry unusual value. Market comps help set expectations, but weak comps create false confidence if the compared businesses had better retention, cleaner financials, or lower platform risk. Strategic value can exceed a financial buyer’s model if your brand fills a category gap, brings access to a customer segment, or gives the acquirer supply chain or channel advantages they do not already have.

Here’s the video version if you want a fast walkthrough before a broker conversation:

That strategic layer is where founder judgment matters. If the likely buyer pool includes aggregators, strategic operators, or capital partners from a curated list of e-commerce investors, the same business can produce very different bids depending on what problem it solves for them after close.

I see the same mistakes repeatedly.

Founders anchor on revenue instead of cash flow. Buyers care about what falls through after ad spend, returns, merchant fees, discounts, freight, payroll, and working capital pressure.

They pitch upside before they prove the base case. Upside only gets paid for after the existing earnings are believable.

They focus on headline price and miss the financial engineering inside the deal. A higher number with an earn-out, inventory adjustment, seller note, or broad indemnity package can be worse than a lower price with more cash at close and tighter terms.

The best valuation case is disciplined and hard to argue with. Clean earnings. Measured add-backs. A clear explanation for why the multiple should hold up under diligence. That is how founders build an asset buyers compete for, instead of a job they agree to take over.

A lot of founders think the goal is to find a buyer. Instead, the objective is to find the right buyer for your asset, your timeline, and your tolerance for post-close entanglement.

That matters even more because the backdrop is still attractive. The global e-commerce market is projected to reach $7.89 trillion by 2028, and the B2B e-commerce segment is valued at $32.11 trillion in 2026, based on projections and estimates compiled by Flowlu’s ecommerce market statistics overview. That kind of scale keeps strategic buyers, financial buyers, and operators active in the market. But they don’t buy for the same reasons.

| Buyer Type | Primary Motivation | Typical Valuation Multiple | Common Deal Structure |

|---|---|---|---|

| Financial buyer | Cash flow, operational improvement, portfolio return | Depends on perceived risk and quality of earnings | Often includes cash at close, sometimes with earn-out or seller support |

| Strategic buyer | Synergy, category expansion, channel access, supply chain advantage | Can stretch above a purely financial view if the fit is strong | Flexible, often tailored around integration needs |

| Individual operator | Ownership of a working business they can run or grow | Usually more conservative unless the asset is exceptionally simple and transferable | Simpler structures, often with transition support |

The “typical valuation multiple” column is qualitative here for a reason. Multiples vary with fundamentals, not buyer labels alone.

A financial buyer usually looks hardest at earnings quality, operational risk, and what they can improve after takeover. They tend to be disciplined. That can be good if your business is clean, because they move from a known playbook. It can be frustrating if your story relies heavily on brand vision or category expansion they don’t underwrite.

A strategic buyer is often where premium outcomes happen. If your business gives them customer access, a product wedge, channel reach, or an operational advantage they don’t already have, they may pay beyond what a pure cash-flow buyer would justify. The trade-off is complexity. Strategic buyers often run slower, involve more stakeholders, and are very concerned about integration risk.

An individual operator can be a strong fit for smaller or simpler businesses, especially if your business is highly transferable and doesn’t require institutional process. These deals can be more personal and more straightforward, but buyer capacity and financing constraints can become issues.

If two buyers offer similar headline numbers, take the one whose model needs your business less to be “fixed” after closing.

Founders fixate on price because it’s easy to compare. Structure is where economics get real.

Common structures include:

An earn-out isn’t automatically bad. In some cases, it bridges a gap between your ask and the buyer’s underwriting. But it only works when the performance metrics are clearly defined, the buyer controls are limited, and your ability to influence the outcome after close is realistic.

Seller financing can help widen the buyer pool and increase flexibility, but it also means you remain exposed. If the buyer struggles operationally, your paper can become a problem.

A founder with a strong brand, differentiated product, and obvious strategic adjacency should not market the deal the same way as a stable but undifferentiated cash-flow business. The outreach, pitch, and negotiation posture should fit the asset.

If you’re trying to map likely acquirers before hiring an advisor, a curated list of e-commerce investors can help you understand who is active in the category and what kind of capital is looking at ecommerce opportunities.

The cleanest process usually creates optionality. More than one credible buyer. More than one viable structure. Enough competitive tension that the discussion shifts from “Will someone buy this?” to “Which path gives me the best combination of certainty, price, and freedom after close?”

Here, founders either justify the valuation or watch it erode.

Due diligence isn’t just a buyer checklist. It’s a stress test of whether your business is real, understandable, and transferable. If your materials are disorganized, if the numbers need too much verbal explanation, or if every answer reveals another dependency, buyers start lowering risk through price cuts, holdbacks, tighter reps, or slower movement.

The founders who handle diligence best don’t “respond well” to questions. They preempt them.

A serious data room should make a buyer feel the business is run by adults.

That means clean folders, current files, obvious labeling, and a structure that follows how buyers think. Financials. Legal. Operations. Marketing. Suppliers. Team. Technology. Inventory. Customer data. If you make someone hunt for basic answers, they’ll assume the hidden issues are worse than the visible ones.

For ecommerce specifically, marketing data gets much more scrutiny than many founders expect. Buyers conduct detailed due diligence on marketing performance, and “presentable, digestible data” matters. The core analytics package should include SEO strategy, CTR analysis, email marketing performance, and SMS engagement rates, as outlined in SmartBug Media’s guidance on selling an ecommerce business.

You don’t need a glamorous setup. You need a useful one.

Include materials like these:

For a stronger framework, this acquisition due diligence checklist for founders is a practical reference.

Raw exports don’t build confidence. Interpretation does.

If CAC has changed, explain why. If margins compressed for a period, show whether it came from freight, promo strategy, or channel mix. If repeat purchase improved, connect it to a system rather than a lucky quarter. A good diligence package gives context without sounding defensive.

The strongest presentation style is simple:

That format works for margin, retention, inventory efficiency, email contribution, or ad performance. It also keeps your team from overtalking in management calls.

Clean analytics reduce uncertainty. Reduced uncertainty usually shows up in either a stronger price, smoother process, or both.

By the time diligence starts, many founders think the hard part is done. It isn’t. Their influence can then wane.

Negotiation goes sideways when sellers become emotionally attached to closing at any cost. Buyers can feel that immediately. The answer isn’t to posture. It’s to know your red lines before the pressure hits.

Protect these points carefully:

When a buyer raises an issue, separate signal from tactic. Some diligence questions expose real weaknesses you must solve. Others are negotiation tools designed to test whether you’ll concede value just to keep momentum.

Momentum matters because stalled deals invite new doubt. But speed without control is expensive.

Set expectations for response time. Centralize buyer communication. Keep one source of truth for documents and revisions. If you have multiple interested parties, maintain enough process tension that no single buyer feels you’ve become captive.

The founder’s job during diligence is to stay factual, calm, and hard to shake. If you do that, diligence becomes a confirmation exercise instead of a discounting exercise.

The LOI feels like a finish line. It’s really permission to start the hardest legal and economic work.

This stage narrows from broad business quality to precise language. What exactly is being sold. What’s excluded. What representations you’re making. How escrow works. What happens if inventory or working capital lands outside the expected range. Small wording changes here can materially change your outcome.

Once you sign the LOI, move fast but don’t get sloppy. Your attorney and tax advisor matter more here than they did in the early sale prep stage.

The big items usually include:

The headline number can still change in effect even if it doesn’t change in name. A deal with a large escrow, broad indemnities, aggressive working capital target, and burdensome post-close obligations is not the same as a clean deal at the same nominal price.

This is the part founders underestimate.

Earlier conversations focus on valuation. Final documents focus on who bears risk if something turns out differently after close. Buyers want broad protection. Sellers want finality. The answer lives in careful drafting, not in vague trust.

A few practical points matter a lot:

The founders who feel best after closing are rarely the ones who “won” every point. They’re the ones who understood exactly what they agreed to.

A messy transition can damage earn-outs, staff morale, supplier continuity, and your own peace of mind.

The handoff should be planned operationally before the wire hits. Who gets told first. Which vendor introductions happen when. How credentials transfer. How customer service continuity is protected. Which team members stay close to the buyer during the first phase. If you’re remaining involved for a transition period, define communication cadence and decision rights early.

A clean transition usually includes:

Most sale advice ignores the personal side. That’s a mistake.

Founders often spend years wiring themselves into every function of the business. Once the transaction closes, the sudden loss of urgency, identity, and control can be disorienting even when the exit is financially strong. If you haven’t thought about what you’re moving toward, not just what you’re leaving, the transition can feel hollow.

So decide early whether you want rest, a new build, investing, advisory work, or a clean break. Don’t leave that question until after close. A successful sale isn’t just cash in the bank. It’s a transition you can live with.

A lot of the actual questions show up in the gray areas. Not valuation theory. Not generic exit timelines. The uncomfortable details founders run into once the process gets real.

If your business is simple, small, and highly transferable, a direct process can work. If the business has meaningful complexity, multiple channels, inventory nuance, cross-border issues, or founder-heavy adjustments, an experienced advisor usually earns their keep.

The biggest value isn’t just finding buyers. It’s managing positioning, process tension, diligence flow, and document-to-document continuity. Founders who sell themselves often underestimate how much value leaks when the buyer controls the pace and frames every issue as a discount.

Much more than most founders expect.

As ecommerce M&A has matured, buyers have become more focused on working capital, subscription models, retention metrics, EBITDA normalization, and CAC payback periods, not just top-line growth, as noted in Bain’s analysis of the gaps in standard ecommerce selling advice.

That means a founder who can explain how cash converts, how customers repeat, and how acquisition spend pays back will usually be taken more seriously than one who only presents revenue growth and ad screenshots.

Later than your emotions want, earlier than the transition requires.

You need confidentiality while the process is uncertain. But you also need enough time to retain key operators and transfer confidence once the deal becomes real. Usually, the right move is to tell a very small circle of critical people only when their involvement becomes necessary for diligence or transition planning.

Don’t turn a possible deal into company-wide anxiety. But don’t spring the sale on essential team members after signatures if their trust is central to continuity.

Assume that possibility from day one.

An LOI is not cash. Deals die in diligence, financing, legal review, or because the buyer loses conviction. That’s why you should keep running the business hard, maintain optionality where possible, and avoid behaving as if the exit is already complete.

A broken deal hurts less when your financials stay current, your process remains organized, and you haven’t mentally spent the proceeds.

Sometimes yes. Often only with caution.

An earn-out can bridge a valuation gap and help get a deal done. But you should only accept one if the metric is tightly defined, the reporting is transparent, and the buyer cannot easily change the rules after closing through budget cuts, channel decisions, or team changes.

If the earn-out depends on variables you won’t control, treat it as uncertain value, not guaranteed price.

Earlier than most founders do.

Tax planning done after the documents are largely set is usually limited planning. Tax planning done before structure is finalized can materially change your outcome. If that’s an area you haven’t pressure-tested yet, this resource on how to reduce your capital gains tax can help frame the questions to take to your own tax advisor.

Yes, but dependence changes both valuation and terms.

Founder dependence doesn’t always kill a deal. It usually changes the buyer pool, lowers confidence, and increases the odds of transition-heavy structures. If you’re still central to supplier relationships, marketing judgment, or daily approvals, expect the buyer to either discount the price or demand more support after close.

The fix is not pretending dependence doesn’t exist. The fix is documenting where it exists and reducing it before market.

If you want to compare notes with founders who’ve already been through complex exits, acquisition talks, and post-close transitions, Million Dollar Sellers is where serious ecommerce operators share the unfiltered playbooks that usually never make it into public content.

Join the Ecom Entrepreneur Community for Vetted 7-9 Figure Ecommerce Founders

Learn MoreYou may also like:

Learn more about our special events!

Check Events