Chilat Doina

May 1, 2026

You’ve already done the hard part. You built one ecommerce brand far enough to learn what drives margin, what breaks fulfillment, how paid media gets noisy, and why a single hero SKU can turn from asset to fragility fast.

Then the ceiling shows up.

Sometimes it looks like channel concentration. Sometimes it’s supplier dependence, platform risk, customer fatigue, or a category that still throws off cash but no longer deserves all of your ambition. That’s usually the moment founders start asking the right question. Not “How do I squeeze more out of this one brand?” but “How do I build a machine that can own several?”

A founder who owns one good brand usually thinks like an operator. A founder who’s building an ecommerce holding company has to think like a capital allocator.

That shift changes everything. You stop asking whether every problem should be solved inside one business. You start asking whether the next unit of time, talent, and cash belongs in the current brand, a new product line, or a separate acquisition altogether. That’s a different game, and it rewards different instincts.

A single brand can produce strong cash flow and still be a weak long-term vehicle. If too much enterprise value sits inside one customer base, one channel, one founder, or one supplier relationship, you don’t have a platform. You have a concentrated asset.

The holdco model fixes that by design.

You create a parent entity that owns multiple operating businesses. Each brand keeps its customer-facing identity, but the portfolio shares the expensive parts that don’t need to be rebuilt every time. Finance, leadership oversight, paid media talent, analytics, inventory planning, agency management, recruiting, and vendor relationships can all move upstream.

That’s where scale starts to matter. Not because “bigger” sounds impressive, but because duplicated effort kills returns.

This isn’t a niche play happening in a tiny corner of online retail. The global ecommerce market reached approximately $6.8 trillion in 2025 and is projected to grow to $8 trillion by 2027, with around 2,685 new ecommerce websites launching daily, according to these ecommerce market statistics. If you’re building an acquisition engine, that matters. It means more brands get created, more subscale founders hit decision points, and more opportunities emerge for buyers who can integrate well.

Practical rule: Build the holdco when your advantage is no longer just product judgment. Build it when your advantage is repeatable brand scaling.

The opportunity is broad enough to support different portfolio theses. You can buy within one vertical and dominate a customer segment. You can build across adjacent categories and cross-sell intelligently. Or you can assemble a diversified portfolio that lowers exposure to any one trend cycle.

The founder has to stop being the hero of every decision. That’s where many otherwise capable operators stall.

In a single brand, founder involvement can hide inefficiency. In a portfolio, it creates bottlenecks. You need systems that survive your absence, reporting that surfaces risk early, and leaders who can run brand-level execution without waiting for your opinion on every landing page or purchase order.

The shift usually looks like this:

From channel tactics to portfolio logic

Instead of obsessing over one Meta account or one marketplace ranking, you compare capital deployment across brands.

From managing people to designing accountability

The question stops being “Who reports to me?” and becomes “Which decisions live at holdco, and which stay inside the brand?”

From maximizing revenue to maximizing enterprise value

A holdco can justify decisions that a single-brand founder often avoids, including category diversification, asset protection, and deliberate centralization.

Owning several brands isn’t the same as operating a holding company. Plenty of founders collect stores and create chaos.

A real holdco has a point of view about what stays centralized and what stays local. Brand voice should stay close to the customer. Cash controls should not. Creative testing can happen inside the brand. Vendor payment controls should not. The best groups create shared capability without flattening what made each brand work.

That’s the unwritten rule. If every acquisition gets fully absorbed into one generic machine, you lose nuance. If nothing gets integrated, you lose advantage.

Building an ecommerce holding company works when you know the difference.

Bad structure makes good deals look bad later. Most portfolio headaches don’t start with the acquisition. They start with loose entity setup, messy banking, and accounting that can’t answer basic questions fast.

If you’re serious about building an ecommerce holding company, the legal and financial foundation has to be clean before the first deal closes. Retrofitting structure after multiple acquisitions is expensive, distracting, and usually tied to some avoidable compliance problem.

Most founders start with an LLC because it’s simple, flexible, and useful for liability protection and pass-through taxation. That’s also the standard guidance in this ecommerce business formation resource, which also emphasizes obtaining separate EINs and separate bank accounts for each entity.

For a self-funded or closely held group, that often makes sense.

A C corporation can become more relevant if you expect institutional investors to enter later, if you want a structure that many professional investors are already comfortable underwriting, or if your long-term plan includes a more formal equity program across leadership. The trade-off is complexity. You’re taking on a more rigid structure earlier, often before the business has earned it.

A practical approach:

| Structure | Where it fits | Main upside | Main trade-off |

|---|---|---|---|

| Parent LLC | Founder-led holdcos, early acquisitions, cash flow focus | Flexibility, simpler governance, pass-through treatment | Can get awkward if future outside capital wants a different setup |

| C corporation | Investor-backed platform builds, formal equity planning | Familiarity for many investors, scalable equity framework | More administration, less flexibility for many founder-operators |

The right answer depends on your capital plan, not on what sounds impressive.

Every operating company should have its own legal entity, its own EIN, and its own bank account. This is not paperwork theater. It’s how you preserve liability boundaries, produce usable financials, and avoid contaminating one business with another brand’s mistakes.

The founders who get in trouble rarely have bad intentions. They just move money casually between entities until no one can tell what actually happened.

At minimum, keep these lines clear:

If your bookkeeper can’t explain where a payment belongs without asking three people on Slack, your structure isn’t ready.

Most founders model acquisitions too narrowly. They forecast brand revenue, gross margin, and ad spend, then ignore the holdco layer that determines whether the portfolio compounds.

Your model needs to show at least three views of the business:

Brand-level P&L

What each operating company earns on its own.

Holdco-level expenses

Leadership payroll, shared software, legal, finance, recruiting, and centralized agency or contractor costs.

Consolidated view

The complete picture after management fees, intercompany charges, and debt obligations.

There are several workable approaches. What matters is consistency.

Some holdcos charge operating companies a management fee. Others absorb central costs at the parent level and judge performance on consolidated cash generation. Some use intercompany loans to fund working capital or inventory builds, especially when one brand produces more free cash than another.

What doesn’t work is improvising every month.

Use a framework like this:

Once you operate across multiple states, with multiple entities and separate obligations, “we’ll handle it later” turns into missed filings and avoidable cleanup work. Keep every entity in good standing, maintain a repeatable document trail, and make sure whoever runs finance has visibility across the entire structure.

That’s the unglamorous side of building an ecommerce holding company. It’s also where disciplined operators separate themselves from founders who are just stacking brands under one umbrella and hoping the back office catches up.

The best deals usually don’t arrive as polished listings. They emerge from a process.

Founders who buy well don’t wait for brokers to hand them obvious assets everyone else has already seen. They build a deal engine. That engine pulls opportunities from direct outreach, peer networks, service-provider referrals, aggregator fatigue, founder burnout, and category-specific relationships that never show up on open marketplaces.

Brokers are useful, but they’re only one lane. If your pipeline depends on broker decks, you’ll spend too much time reviewing businesses that have already been mass-marketed.

A better sourcing mix looks like this:

Direct founder outreach

Go after operators in categories you understand. Many owners won’t list publicly but will respond to a buyer who sounds credible and specific.

Private operator networks

Accountants, agency owners, 3PL operators, and top-tier freelancers often know who’s tired, overextended, or considering a sale.

Category adjacency

The best bolt-on targets often sell to the same buyer with a different product set. Those founders are easier to underwrite because you already understand the customer.

Marketplace and channel pattern recognition

If you know how to read a category, you can often spot under-managed brands through product presentation, pricing discipline, inventory behavior, and review cadence.

Don’t build your pipeline around “businesses for sale.” Build it around “founders who might be ready.”

A good target doesn’t just have revenue. It has transferability.

The first pass should answer five questions fast:

Can demand survive the seller’s exit?

If the founder is the face, the operator, the media buyer, and the product developer, you’re not buying a business. You’re buying a job with a transition risk.

Is the brand differentiated enough to defend margin?

If the offer is generic and the creative is the only moat, assume pressure will show up as soon as you scale.

Can supply hold under ownership change?

You need to know who controls the production relationship, lead times, and quality.

Are the customers worth keeping?

Repeat behavior, brand affinity, and product fit matter more than top-line vanity.

Will the asset integrate into your portfolio without creating a custom mess?

Every acquisition shouldn’t require a unique tech stack, custom reporting logic, and a fresh operating model.

The fastest way to lose money in acquisitions is to fall in love with narrative before checking mechanics. Review financials, but don’t stop there. Ecommerce deals fail in operations, customer concentration, inventory quality, and platform dependency just as often as they fail in accounting.

If you want a broader external reference, this expert guide for M&A due diligence is a useful companion to an internal operating checklist.

Here’s a practical version built for ecommerce operators:

| Category | Check Item | Why It Matters |

|---|---|---|

| Financials | Revenue by channel | Channel concentration changes risk fast |

| Financials | Margin by product family | Some “growth” hides low-quality SKU mix |

| Financials | Add-backs and owner expenses | Inflated adjustments distort real earnings |

| Customer | Returning customer behavior | Shows whether demand is transactional or brand-led |

| Marketing | Creative dependency | If one ad angle carries the business, performance can break quickly |

| Marketing | Attribution logic | Inconsistent tracking creates fake confidence |

| Operations | Supplier concentration | One fragile vendor can become your main post-close problem |

| Operations | Inventory aging | Old stock can silently destroy deal economics |

| Technology | Store apps and systems sprawl | Tool overload complicates migration and reporting |

| Legal | Trademark ownership | If IP isn’t clean, the asset isn’t clean |

| Legal | Contractor and employee agreements | Hidden people risk creates transition issues |

| Brand | Review profile and customer complaints | Recurring complaints point to product or fulfillment defects |

| Platform | Account health | Policy issues can become immediate revenue threats |

For a deeper transaction-specific operating template, keep a dedicated acquisition due diligence checklist for ecommerce deals in your internal process library. The point isn’t the document itself. The point is forcing the same discipline on every target.

Some issues can be fixed after closing. Some should kill the deal.

Walk away, or heavily reprice, when you see patterns like these:

The best acquisition isn’t always the most interesting brand. It’s the one your system can improve without distorting what customers already like.

That means you should prefer targets where your team already knows how to help. If your edge is merchandising and supply chain, don’t buy an asset that requires deep subscription retention expertise on day one. If your edge is Amazon, be careful with brands whose value depends on founder-led DTC storytelling.

A holdco gets paid for repeatability. The cleaner the fit between your capabilities and the target’s gaps, the better the deal usually is.

A lot of buyers obsess over valuation and still structure weak deals. Price matters, but structure decides who absorbs risk, how cash moves, and whether the business can survive its own acquisition.

Experienced buyers don’t ask only, “What is this worth?” They ask, “What should be paid now, what should be paid later, and what has to be proven before more money changes hands?”

Most deals are a mix of four building blocks.

Cash at close

Clean and simple. Sellers like it. Buyers lose flexibility.

Seller financing

Useful when you want the seller aligned and when you don’t want to overuse your own cash or debt capacity.

Performance-based earnout

Smart when future results depend on a seller handoff, customer retention, product continuity, or a key growth thesis that hasn’t been proven yet.

Stability or transition payments

Helpful when the seller is staying involved for a limited period and you need continuity across supplier relationships, key accounts, or operational transfer.

None of these terms is good or bad on its own. The right mix depends on the fragility of the business and your confidence in post-close execution.

Seller financing is attractive because it lowers the cash burden up front and keeps the seller economically tied to the outcome. It also exposes a useful truth. A seller who insists on full certainty while asking you to absorb all transition risk is telling you something about their confidence.

That said, seller paper only works if the company’s cash generation can service the obligation without starving inventory, advertising, and working capital. Founders get into trouble when they buy a solid asset and then strip it of operating flexibility to meet aggressive payment schedules.

A deal that looks conservative on paper can still be reckless if the business needs oxygen right after closing.

All-cash offers can win competitive situations and reduce legal friction. They’re also useful when the asset is clean, the handoff is straightforward, and you want total control without seller entanglement.

The downside is obvious. You’ve concentrated risk in a single moment. If diligence missed something operational, your recourse is narrower and your capital is already gone.

That’s why the best buyers tie structure to uncertainty. The more transition risk, the more contingent the structure should become.

There isn’t one correct funding path. There is only the one that fits your portfolio strategy and your tolerance for downside.

A simple comparison helps:

| Capital source | Best use case | Main advantage | Main caution |

|---|---|---|---|

| Self-funding | First acquisitions, high control buyers | No external approval layer | Limits deal pace and diversification |

| Bank or acquisition debt | Stable businesses with predictable cash generation | Preserves equity ownership | Payment obligations reduce flexibility |

| Private investors | Faster portfolio build, larger opportunities | Expands buying power and network | Governance gets more complex |

| Seller financing | Higher-trust deals, transition-heavy businesses | Aligns incentives, lowers cash at close | Terms can still strain cash flow |

If you’re weighing ownership dilution against repayment pressure, this breakdown of equity financing vs debt financing is a useful way to think about the trade-offs.

One reason the holdco model deserves serious attention is that it has clear real-world precedent. 365 Holdings grew a six-brand portfolio starting with a single acquisition in 2017, which supports the case for deliberate, repeatable acquisition strategy rather than one-off dealmaking, as detailed in this profile of 365 Holdings and Kelcey Lehrich.

That’s how strategic portfolio builders think. They don’t need every deal to be perfect. They need a structure and capital approach they can repeat.

Start with the business’s transfer risk, not with ego.

If the company relies heavily on seller relationships, reduce cash at close and increase contingent payments. If inventory quality is uncertain, protect yourself with holdbacks or specific working capital terms. If the transition is light and the systems are mature, simplify.

A strong offer usually does three things well:

The founders who build strong portfolios aren’t just good at buying. They’re good at keeping the acquired company healthy after the purchase.

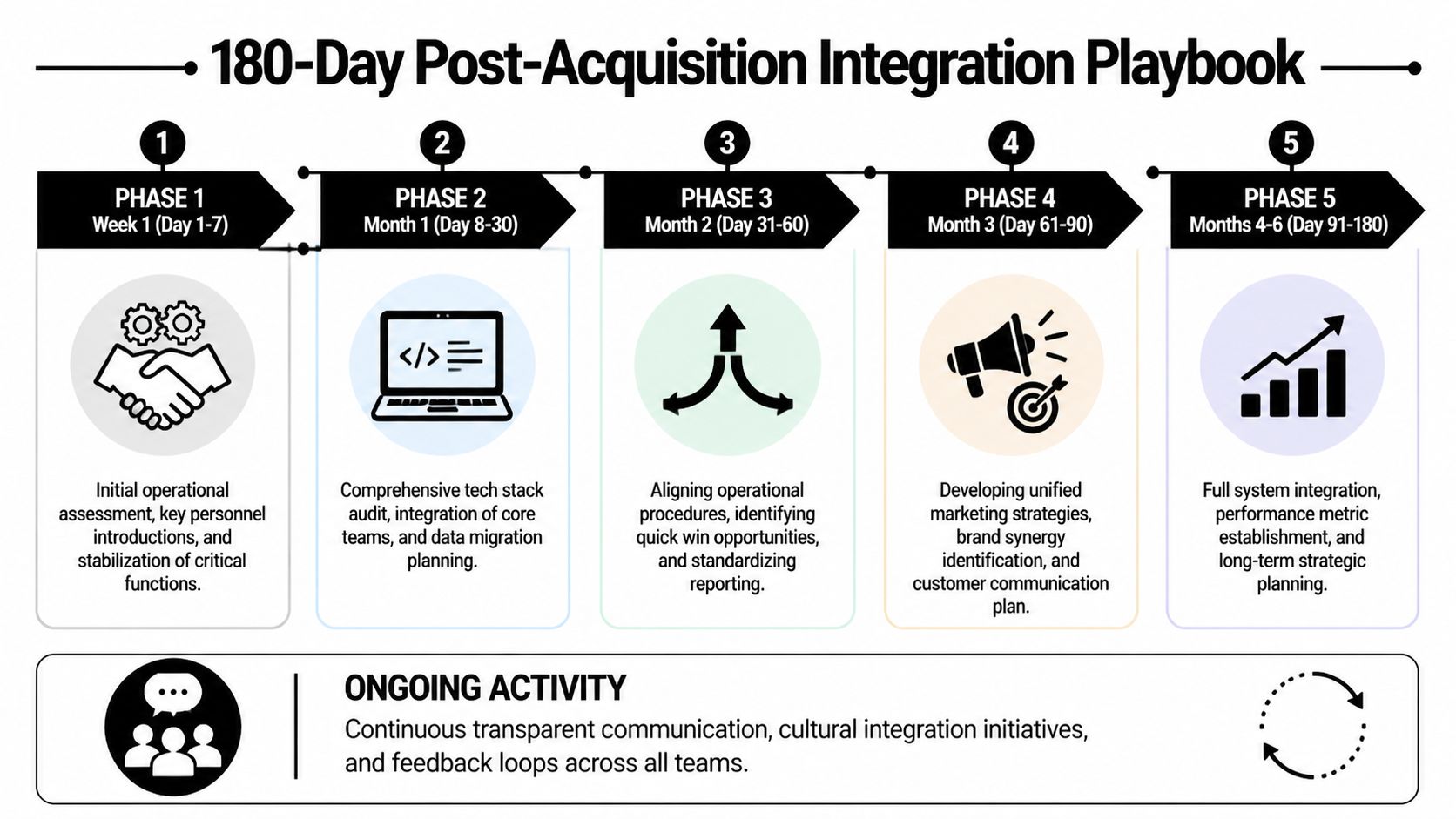

Most acquisition value is won or lost after the paperwork. The mistake is thinking integration means immediate standardization. It doesn’t. The first job is stabilization. The second is visibility. Standardization comes after you know what can be changed without damaging what made the brand worth buying.

Use the first half-year to sequence decisions, not to force them.

The new brand doesn’t need a revolution in week one. It needs continuity.

Protect the essentials first. Keep orders moving. Keep customer service live. Keep ad accounts, marketplace listings, payment processors, supplier communications, and key team routines functioning without interruption. If something is messy but operational, document it before changing it.

Your first month should focus on three tracks:

Operator mapping

Identify who performs the work, not who appears on the org chart.

Cash and inventory control

Reconcile open POs, inventory position, supplier terms, and immediate payables.

System audit

Review the stack, including storefront tools, reporting, email platform, ad account access, analytics, and product data storage.

At this point, most holdcos either gain advantage or create confusion.

You need common reporting, common definitions, and common operating rhythms. If one brand defines contribution margin differently, another closes books late, and a third tracks inventory with ad hoc spreadsheets, you don’t have a portfolio. You have separate companies with a shared owner.

For this phase, documented process matters more than speed. Build and enforce clear standard operating procedures for scaling teams, especially around purchasing, content publishing, promotions, returns, and financial close.

The best integration isn’t the fastest one. It’s the one that creates consistency without interrupting momentum.

A practical weekly review cadence during this period should include:

By this stage, you should know what belongs at holdco and what should remain embedded in the brand.

This is also where technical architecture starts paying off. A serious portfolio often needs systems that support both D2C and B2B, including tools like CPQ and PIM, because product information, quoting, invoicing, and channel-specific workflows eventually have to behave consistently across brands. That need is outlined in this guide to manufacturing ecommerce infrastructure.

A useful integration lens is simple:

| Keep brand-specific | Centralize at holdco |

|---|---|

| Voice, positioning, creative nuance | Finance controls and reporting |

| Product strategy by customer segment | Shared data definitions |

| Community and customer communication style | Vendor management standards |

| Brand-level merchandising judgment | Core tooling decisions where practical |

The timeline below is worth reviewing with your operators before any integration sprint begins.

Founders create integration damage in predictable ways:

A clean integration playbook respects two truths at once. The acquired company must change enough to fit the portfolio. It must also stay recognizable enough to preserve what customers were already buying.

A portfolio becomes real when the founder stops being the operating system.

In the early phase, that founder can still personally arbitrate hiring, approve spend, jump into vendor calls, and rescue weak operators. As the group matures, that behavior starts lowering value. Buyers don’t pay top dollar for a collection of businesses that only function because one person knows where everything is buried.

The holdco starts with a few practical roles, not a bloated headquarters.

You need someone who owns finance discipline across the group. You need brand-level leaders who can run weekly execution. You need a central operator, or operators, who can drive process across inventory, reporting, and performance management. You do not need a giant executive layer pretending to be public-company management.

A strong portfolio setup often separates responsibilities this way:

That arrangement matters because it creates accountability where it belongs. The brand manager owns the result. The holdco team owns the environment and the standards.

A useful holdco dashboard doesn’t overwhelm. It forces comparability.

Every brand should report the same core set of operating metrics using the same definitions. The exact KPI stack varies by business model, but the discipline does not. If one brand can’t close cleanly, or another can’t explain inventory health in the same language as the rest of the portfolio, governance is still immature.

Buyers trust portfolios that can explain performance clearly, repeatedly, and without founder interpretation.

At this stage, capital allocation gets sharper. Some brands deserve additional inventory, leadership upgrades, and growth investment. Others should be optimized for cash generation. A few should probably be sold, wound down, or left alone while better opportunities absorb management attention.

Most maturing holdcos grow through one of three paths.

One path is bolt-on acquisitions that deepen an existing category. Another is shared-customer expansion, where your current audience gives you permission to add adjacent brands. The third is channel or geography expansion, but only after the operating core is already disciplined.

Not every growth lever deserves the same weight. If the portfolio still depends on founder escalation and custom reporting, acquisition pace should slow. If your controls are strong, your integration playbook works, and your team can absorb new assets without drama, you can press harder.

For operators looking to sharpen the commercial side of that equation, these strategies for measurable ecommerce growth are a useful external perspective on how to think about sustained brand expansion once the operational base is solid.

Exit value is shaped long before a banker enters the process.

A discerning buyer wants clean legal ownership, reliable financial reporting, repeatable integration history, defendable margins, and leadership depth that survives the founder stepping back. They also want a portfolio thesis that makes sense. Not random brand accumulation. Coherent ownership.

That’s why building an ecommerce holding company is different from buying a few stores and hoping scale shows up. Value sits in governance, transferability, reporting quality, and the discipline to allocate capital where the portfolio earns the best return.

If you get that right, you don’t just own multiple brands. You own a platform that someone larger can underwrite with confidence.

If you're already operating at a serious level and want to learn from founders who’ve built, bought, and scaled ecommerce brands in practice, Million Dollar Sellers is where those conversations happen. It’s an invite-only community for high-level operators who value trusted peer insight, hard-won execution lessons, and practical strategies that move enterprise value, not just vanity metrics.

Join the Ecom Entrepreneur Community for Vetted 7-9 Figure Ecommerce Founders

Learn MoreYou may also like:

Learn more about our special events!

Check Events