Chilat Doina

May 22, 2026

A founder signs an LOI, takes a mix of cash and future consideration, and tells the team they've de-risked the business. Months later, the buyer is in distress, payouts are delayed, and the part of the purchase price that looked safest on paper becomes the most uncertain piece of the deal.

That's the true reason Thrasio still matters.

For a stretch of the ecommerce boom, Thrasio represented the cleanest possible exit narrative for Amazon sellers. Build a strong FBA brand, get noticed by an aggregator, sell at a compelling multiple, and let a better-capitalized operator take over the next phase of growth. It felt rational to both sides.

Sellers saw a buyer class that appeared professional, well funded, and structurally built to scale assets they could no longer optimize alone. Investors saw a fragmented market of third-party Amazon brands and a roll-up machine that promised to centralize sourcing, advertising, logistics, and analytics. Operators saw a shortcut to portfolio scale without incubating every brand from zero.

That dream had a strong logic. It also had a dangerous assumption buried inside it. The assumption was that financial capacity and operational capacity were roughly the same thing.

They aren't.

Thrasio became the symbol of that mismatch. At its peak, it looked like proof that Amazon-native M&A had matured into a legitimate asset class. In hindsight, it looked more like a stress test of whether a marketplace-native roll-up could absorb complexity faster than complexity absorbed it.

For founders who lived through that market, the important question isn't just “what happened to Thrasio?” It's what its trajectory revealed about the hidden fragility of aggregator exits.

If you want context for why the holding-company model looked so compelling in the first place, this breakdown of building an ecommerce holding company is useful background. The model itself was never irrational. The problem was how aggressively some players tried to run it.

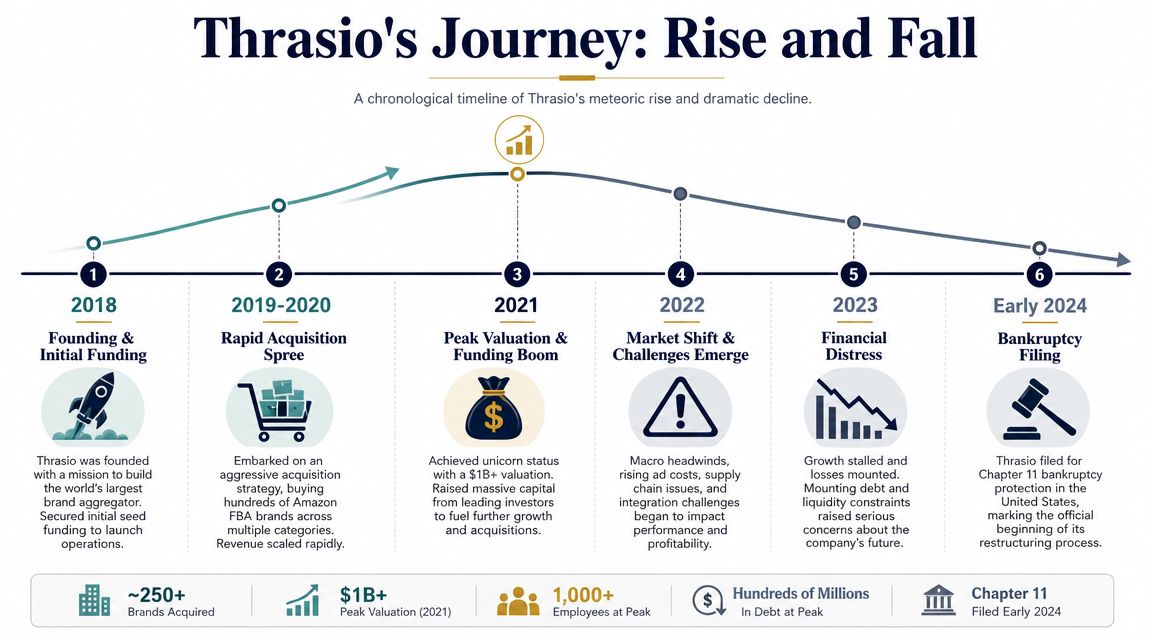

For a period, Thrasio looked less like a buyer and more like the clearing price for an entire asset class. A founder with an Amazon brand could point to Thrasio's pace, capital base, and acquisition appetite and infer that marketplace businesses had become institutionally financeable. According to this account of Thrasio's rise and fall, the company was founded in 2018, reached a reported $10 billion valuation, and raised more than $3 billion in capital as it raced to assemble a portfolio of third-party marketplace brands.

The timing mattered. Amazon's third-party ecosystem had already produced a large population of brands with real revenue, strong review profiles, and years of operating history, but many still sat below the size threshold that attracted conventional consumer private equity. Thrasio offered a bridge between founder-owned ecommerce and scaled consumer M&A.

That mattered for sellers because it changed exit expectations. If aggregators could buy quickly, underwrite off marketplace data, and pay on trailing performance, founders no longer had to wait for a strategic acquirer or build a management team to pursue a sale. The rise of Thrasio did more than create liquidity. It reset assumptions around how fast a seller could run a process, what diligence would focus on, and how much post-close risk a founder might be asked to retain through an earnout or inventory true-up.

Once that much capital entered the system, speed stopped being a tactic and became part of the business model. An aggregator financed for rapid consolidation has to keep turning capital into assets, then turn those assets into cash flow quickly enough to support the next round of buying. In practice, that changes how decisions get made inside the acquirer.

The underwriting question shifts from long-term asset quality to integration velocity. A team can know that a brand has concentration risk, supplier fragility, or margin exposure to freight and still move ahead if the machine requires more volume. That is where seller-side analysis gets sharper. A high bid from an aggregator is not always the same thing as high conviction. Sometimes it reflects pressure to deploy capital, defend growth narratives, or fill a category gap before financing terms tighten.

For founders, that distinction carries direct deal implications. If the buyer needs your EBITDA to support its own capital story, your earnout risk goes up. If the platform is onboarding too many brands at once, post-close integration risk shifts back to the seller through working-capital disputes, delayed payments, inventory resets, or aggressive performance adjustments.

The market's reading of Thrasio changed on February 28, 2024, when the company filed for Chapter 11 bankruptcy protection in the U.S. Bankruptcy Court for the District of New Jersey. As noted earlier in the same source, the filing was framed as a restructuring rather than a liquidation.

That difference matters.

A liquidation would have implied the assets were broadly impaired. A restructuring suggested something else. The operating portfolio still had value, but the company's obligations, ownership structure, and execution model were no longer aligned with the economics of running that portfolio.

Thrasio's break was not simply financial. The company appears to have reached a point where acquisition volume, integration capacity, and working-capital demands no longer moved in sync.

That is a more useful interpretation for operators than the standard debt-only summary. Debt amplified the problem. It did not create SKU complexity, supplier coordination issues, channel-level execution gaps, or the internal reporting burden that comes with hundreds of acquired products spread across a single platform.

The second-order effect is easy to miss if you focus only on the bankruptcy headline. Thrasio's rise trained many founders to evaluate buyers by headline multiple, speed to LOI, and access to capital. Its stall exposed a different hierarchy. Buyer quality depends on integration discipline, cash conversion, and portfolio control. Those factors determine whether an acquirer can honor the economics implied in the purchase agreement.

That changes how experienced sellers should read aggregator offers. A buyer with abundant funding but weak operational absorption capacity can still close a deal. The problem shows up later, when earnouts get missed because inventory was mishandled, ad spend was cut, supplier terms deteriorated, or category management attention was spread too thin across the portfolio.

Thrasio's rise proved that aggregators could create a new exit lane. Its halt showed that founders also needed to diligence the buyer. Not just the letter of intent, but the machine behind it.

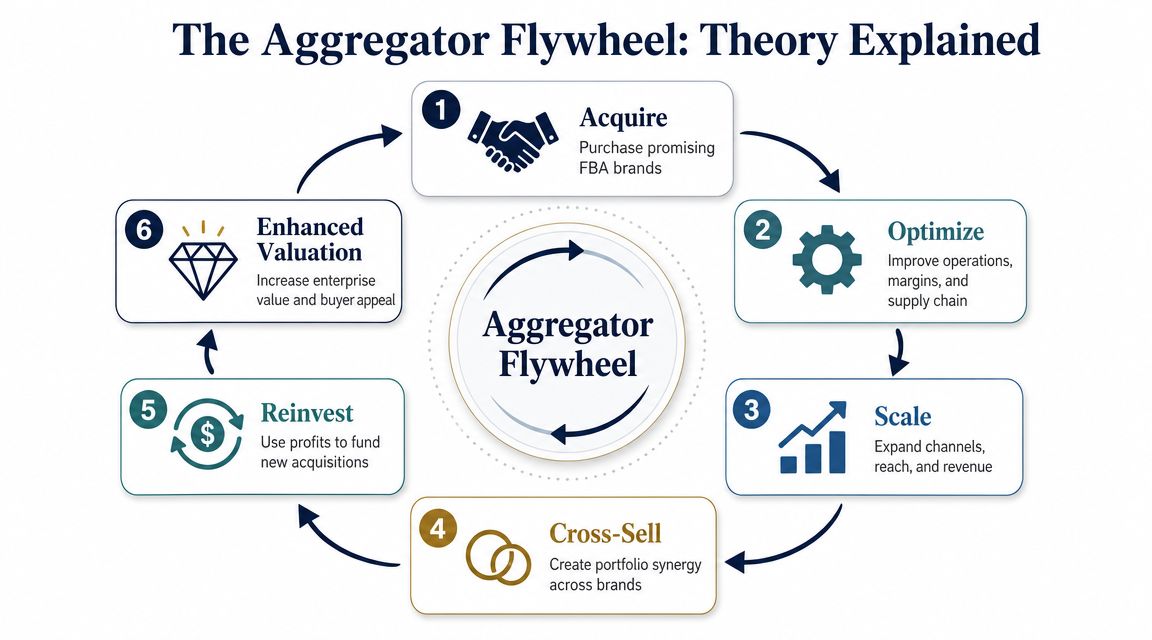

The aggregator model made intuitive sense because it borrowed from a familiar playbook. This resembles a real estate operator buying a scattered portfolio of well-located properties, then improving occupancy, reducing procurement costs, standardizing management, and refinancing the portfolio at a higher enterprise value. In ecommerce, the assets weren't buildings. They were brands, listings, supplier relationships, and contribution margins.

At a high level, the model had six moving parts:

That's the theory. Nothing in that theory is flawed.

For founders, aggregators solved several real problems. Many Amazon-native operators had built solid businesses but lacked senior talent in supply chain, paid media, forecasting, or finance. Others were fatigued by marketplace concentration risk and wanted liquidity without waiting for a traditional strategic buyer.

The aggregator pitch was attractive because it translated founder dependence into institutional process. It told sellers, in effect, “Your brand is good, but it's trapped inside a small system. We'll put it inside a bigger one.”

That promise had emotional force. It allowed founders to believe they weren't selling because they'd hit a ceiling. They were selling because a larger operating platform could realize more value than they could on their own.

Practical rule: Every aggregator pitch rests on a simple claim. The buyer must operate your brand better after closing than you operated it before closing.

The model only works if the acquirer is strong in three areas at the same time:

| Area | What must be true | What breaks if it isn't |

|---|---|---|

| Deal selection | The buyer acquires brands whose economics remain sound after normalization | The portfolio inherits weak assets at inflated expectations |

| Integration | Systems, suppliers, and operating routines can be absorbed without loss of control | Savings stay theoretical while complexity becomes real |

| Capital structure | The company has enough flexibility to hold, fix, and selectively grow brands | Short-term liquidity pressure forces bad operating decisions |

This is why the best version of aggregation was always more operational than financial. Financial engineering can help a good operator. It can't substitute for one.

The flywheel also contains a trap. Each success encourages the next acquisition before the prior one is fully integrated. If the organization believes it has a repeatable playbook, it starts treating variation as noise rather than risk. But Amazon brands vary in category dynamics, review durability, supplier concentration, compliance exposure, and advertising sensitivity.

The moment an acquirer starts assuming all FBA assets are similar, the model begins losing precision.

That's where a lot of operators misread Thrasio. They see a failed roll-up and conclude the model was fantasy. The more accurate reading is narrower. The model works only when acquisition discipline, portfolio architecture, and operating depth stay in balance. Once that balance slips, the same flywheel that drove growth starts amplifying mistakes.

The easiest explanation for Thrasio is that it used too much debt. That's true, but it's also lazy analysis. Excessive debt rarely destroys a business by itself. It destroys a business whose operations can no longer absorb shocks, whose assets take longer to stabilize than financing terms assume, and whose management systems lose fidelity at scale.

A roll-up lives or dies on the quality of what it buys. If an acquirer purchases brands based on temporary performance, incomplete diligence, or optimistic assumptions about post-close improvement, it doesn't just overpay. It imports future operational work at a price that leaves little room for error.

In a fast market, buyers can start underwriting the path to value creation as if it were already captured. That compresses margin for mistakes. It also creates a portfolio filled with assets that require intervention immediately after close.

The problem for a serial acquirer is obvious. If too many brands arrive needing immediate repair, the operating team becomes triage staff rather than growth staff.

Integration risk is usually discussed like an org-chart problem. It's more mechanical than that. Every acquired brand brings suppliers, reorder logic, listing conventions, packaging decisions, refund patterns, and category-specific cadence. Put enough of those into one platform and complexity stops being additive. It becomes combinatorial.

A founder running one brand can often manage exceptions manually. A platform managing many brands cannot. It needs clean systems, consistent decision rights, and reliable operating data. If any one of those is weak, the platform starts creating internal friction faster than shared services can remove it.

For founders evaluating acquirers, this is why diligence has to go beyond valuation and headline funding. The buyer's process maturity matters. A good starting point is a serious acquisition due diligence checklist, not just for the acquirer inspecting you, but for you inspecting the acquirer.

A buyer can have money, talent, and ambition and still fail the handoff if it doesn't have integration bandwidth.

The roll-up strategy was especially vulnerable to external changes because it assumed that improved execution would offset pressure elsewhere. But some pressures don't offset cleanly. They stack.

When freight conditions shift, ad efficiency deteriorates, consumer demand normalizes, or financing becomes less forgiving, portfolio operators lose room to smooth underperformance. A standalone founder can sometimes cut SKUs, slow growth, and preserve cash with brute-force focus. A large aggregator has more moving parts and more fixed commitments. It often can't pivot as quickly because every change ripples through teams, inventory positions, and lender expectations.

This pattern shows up outside Amazon as well. The Awok in UAE story is a useful parallel because it illustrates a broader truth about digital commerce businesses that expand aggressively before their systems are resilient enough. Different company, different context, same analytical lesson: top-line ambition doesn't neutralize operating strain.

The aggregator promise depends on operational uplift. But operational uplift is not infinitely scalable. At some point, management attention becomes the constrained resource.

That matters more than many finance-first analyses admit. Brands don't improve because they sit inside a larger portfolio. They improve because specific people make specific interventions. They renegotiate terms, fix listing issues, adjust forecast logic, revisit packaging, repair inventory flow, and resolve channel conflicts. If the organization spreads strong operators across too many assets, each brand receives less effective stewardship.

That creates a dangerous lag. Portfolio reporting can still look acceptable while brand quality decays.

A later view of the mechanics helps underscore the point:

These weren't isolated problems. They reinforced one another.

That feedback loop is what “what happened to Thrasio?” should mean to experienced operators. The company didn't merely hit a debt wall. It built a system in which acquisition logic, portfolio management, and financing assumptions all depended on the others working smoothly at once. Once the coordination broke, the capital structure had no patience.

The most interesting part of Thrasio's story is that it didn't end in liquidation. It was forced into simplification. That distinction matters because it separates a broken model from a broken company. Some parts of the business still had enough value to support a reset, but only under a very different set of rules.

According to Aura's summary of the restructuring outcome, Thrasio had to eliminate $495 million in debt and secure $90 million in new financing to emerge from Chapter 11. In June 2024, roughly four months after filing, the company exited bankruptcy under a slimmer structure and new leadership, with Stephanie Fox, its first employee and former COO, appointed CEO.

The restructuring terms tell you what creditors and operators believed was salvageable. They did not back a return to the original playbook. They backed a narrower company built around fewer brands and a more controlled operating footprint.

That's the critical point. Survival did not come from doubling down on the acquisition engine. It came from shrinking the system until it could be managed profitably.

In M&A terms, that is a harsh verdict on the earlier strategy. A company that once justified its value through breadth and momentum exited restructuring by emphasizing focus and operating discipline. The platform survived, but the original theory of scale-at-speed did not.

Appointing an insider with operational roots was not a cosmetic move. It suggested that the company needed an execution leader more than a capital-markets story. When a roll-up breaks, the recovery playbook usually becomes highly operational: fewer moving parts, cleaner accountability, tighter SKU and brand prioritization, and a more honest view of what the organization can effectively run well.

The restructuring answer to complexity is rarely cleverness. It's reduction.

That shift has implications beyond Thrasio. It reframes what “institutional quality” should mean in ecommerce M&A. Institutional quality is not just polished diligence materials and financing access. It's the ability to say no to assets, concentrate management attention, and preserve control under stress.

Founders often interpret bankruptcy as a final judgment. In cases like this, it's better read as a forced repricing of strategy. The market withdrew support from one version of the business and funded another one.

That's a familiar pattern in turnarounds. The company that emerges is often built on practices operators could have recognized much earlier: portfolio pruning, cost control, simpler reporting lines, and sharper unit-level accountability. For a non-ecommerce parallel on disciplined overhead management, this primer on actionable cost-cutting for service companies is useful because the principle travels well across business models. When systems get too heavy, recovery starts with stripping them back.

If you're thinking about your own capital stack, the right lens is not just growth financing. It's resilience under bad assumptions. This comparison of equity financing vs debt financing is relevant because Thrasio's restructuring made one point unmistakable: debt can accelerate a strategy, but it also removes time when the strategy needs time most.

A founder sells an eight-figure brand, announces the exit, and assumes the risk transfer is complete. Months later, part of the purchase price depends on a buyer that is missing forecasts, changing operators, and preserving cash. In aggregator deals, that scenario is not edge-case drafting risk. It sits at the center of the transaction.

The seller-side lesson from Thrasio matters more than the buyer-side postmortem. Investors can absorb a failed roll-up inside a portfolio. Founders usually cannot replay a sale process once their brand, team, and payout mechanics are tied to one acquirer. According to this seller-focused analysis of the Thrasio collapse, one of the least examined consequences of the company's distress was what happened to sellers waiting on deferred consideration or disputing post-close payments. That is the point many operators missed during the aggregator boom. A signed LOI did not eliminate risk. It often rearranged it.

Founders often anchor on headline valuation and treat structure as a legal cleanup item. In aggregator transactions, structure determines how much of the price is firm and how much remains exposed to the acquirer's execution, liquidity, and reporting quality.

A few implications follow.

Contingent consideration is not bad. It has to be underwritten as risk-bearing paper, not celebrated as if it were cash.

Aggregator-era buyers sold certainty: repeatable playbooks, centralized expertise, and institutional process. Sellers should have asked a narrower question. Who exactly owns the brand on day 31, and what constraints will that person face?

That changes the diligence list. A polished deck and well-known lenders are weak substitutes for basic operational evidence. Sellers should press on issues such as funding source, payment mechanics, integration ownership, inventory authority, and the reporting definitions that govern earnouts.

| Question | Why it matters | What a weak answer sounds like |

|---|---|---|

| How is the deal funded? | Shows whether payment relies on committed capital, warehouse lines, or future fundraising | “We have strong backing” without specifics on timing or source |

| Who owns integration after close? | Determines whether there is a named operator with authority over inventory, advertising, and supply chain | “Our team handles that” |

| How are earnouts calculated and audited? | Reduces the chance that disputes emerge from definitions, SKU transfers, or reporting gaps | “We'll align after close” |

| What happens if inventory assumptions break? | Tests whether the buyer has a practical replenishment plan or a spreadsheet assumption | “We optimize quickly” without operational detail |

If a buyer cannot explain how your brand will be managed after closing, the issue is not merely weak communication. It is weak underwriting.

Peer references help, but they should be used like diligence evidence, not social proof. Speak with founders who sold into similar structures and ask what changed after close: who made decisions, how often forecasts were missed, whether inventory was funded on time, and how transparent the reporting became once the seller no longer controlled the systems.

Optionality changes negotiating power. A business that can attract strategic acquirers, private equity-backed operators, or continue compounding independently can reject structures that overuse earnouts, rollovers, or seller financing. A business that only fits the roll-up bid set usually cannot.

That is why sellability starts well before a process. Category depth matters. Channel diversity matters. Brand-specific demand matters. So does a management team that can explain margin by SKU, customer cohort, and channel without relying on adjusted narratives.

The common thread is simple. The harder your business is to commoditize, the less likely you are to be priced on an aggregator template.

Operational literacy also affects valuation quality. Freight, lead times, stockout risk, and cash conversion all feed the model a buyer uses to justify price and structure. Sellers who can understand FCL and LCL differences are better positioned to challenge bad assumptions in working-capital targets and inventory forecasts, because freight mode decisions often sit underneath the purchase-price math.

Thrasio exposed a gap between looking institutional and being safe to sell to. Well-produced materials, large capital raises, and acquisition volume can create the appearance of low counterparty risk. For sellers, those signals matter less than a buyer's ability to pay on time, integrate without disruption, and preserve enough liquidity to support the brand after closing.

That distinction has direct implications for exit strategy. The highest LOI is not automatically the best offer. A lower headline price with more cash at close, tighter definitions, cleaner adjustment language, and fewer dependencies on platform-level performance can produce the superior risk-adjusted outcome.

For 8-figure founders, the practical lesson is clear. Underwrite the acquirer with the same intensity they apply to your business. In deals with aggregators, buyer quality is not background context. It is part of the purchase price.

The Thrasio model isn't dead. The undisciplined version of it is.

There will still be acquirers in ecommerce. Fragmented markets always attract consolidation. The difference is that the next generation of buyers will have to win on category expertise, integration rigor, and conservative deal structuring rather than on speed alone. They'll likely buy fewer brands, underwrite them more carefully, and focus on businesses they can operate effectively, not just aggregate.

That shift should be healthy for founders. It may reduce the number of flashy bidders, but it improves the odds that serious buyers are built to own what they buy. In practical terms, the future probably belongs to firms with narrower mandates, clearer operational strengths, and less dependence on financial momentum.

The deeper takeaway from what happened to Thrasio is not that ecommerce roll-ups were a fantasy. It's that operational excellence sets the ceiling for financial engineering. Once an acquirer outruns its ability to integrate, forecast, and manage, the capital structure stops being an advantage and starts becoming a countdown.

Founders should remember that when they build, when they finance, and when they sell. The best businesses still create value the old-fashioned way. They understand their customers, control their operations, and leave themselves room to survive a market that doesn't care about the deck they raised on.

If you're an established ecommerce operator navigating growth, acquisition interest, or a more disciplined exit strategy, Million Dollar Sellers offers an invite-only community where experienced founders compare notes on real operating issues, including deal structure, capital decisions, and what buyers look like behind the pitch.

Join the Ecom Entrepreneur Community for Vetted 7-9 Figure Ecommerce Founders

Learn MoreYou may also like:

Learn more about our special events!

Check Events