Chilat Doina

March 14, 2026

Think of working capital management as the art of juggling your short-term cash flow. It's the day-to-day strategy you use to make sure you have enough cash on hand to pay your bills—like supplier invoices and payroll—while also putting your money to work to grow your brand.

Let's use an analogy. If your business is a high-performance car, revenue is the fuel you pump into the tank. But working capital is the oil. You can have a full tank of gas, but if you run out of oil, the engine will seize up and grind to a halt.

That's exactly what happens when an e-commerce brand runs out of cash.

So, what is working capital management? It's the hands-on process of keeping that engine running smoothly. It's a constant balancing act—you need enough cash to cover your immediate costs, but you don't want too much money tied up in things that aren't earning you a return.

For an e-commerce founder, this isn't just some abstract accounting concept. It's the key to your operational freedom and determines your ability to:

At its core, working capital management comes down to the relationship between what your business owns (current assets) and what it owes (current liabilities) over the next 12 months.

And businesses are paying more attention than ever. The global market for working capital management solutions is expected to jump from US$4.1 billion in 2026 to US$7.3 billion by 2030. This growth shows just how critical it is for brands to get their cash flow right. You can explore the market projections and see for yourself how vital these strategies have become.

To really get a handle on this, we need to break down the moving parts for an e-commerce brand.

Here’s a quick rundown of the main pieces you’ll be dealing with.

This table gives you the basic building blocks. But the real magic isn't just in the numbers themselves—it's in how they interact.

The goal of working capital management isn't just to have more assets than liabilities. It's to optimize the speed at which you convert those assets (like inventory) into cash and strategically manage the timing of paying your liabilities. This dynamic flow is what keeps your business healthy and agile.

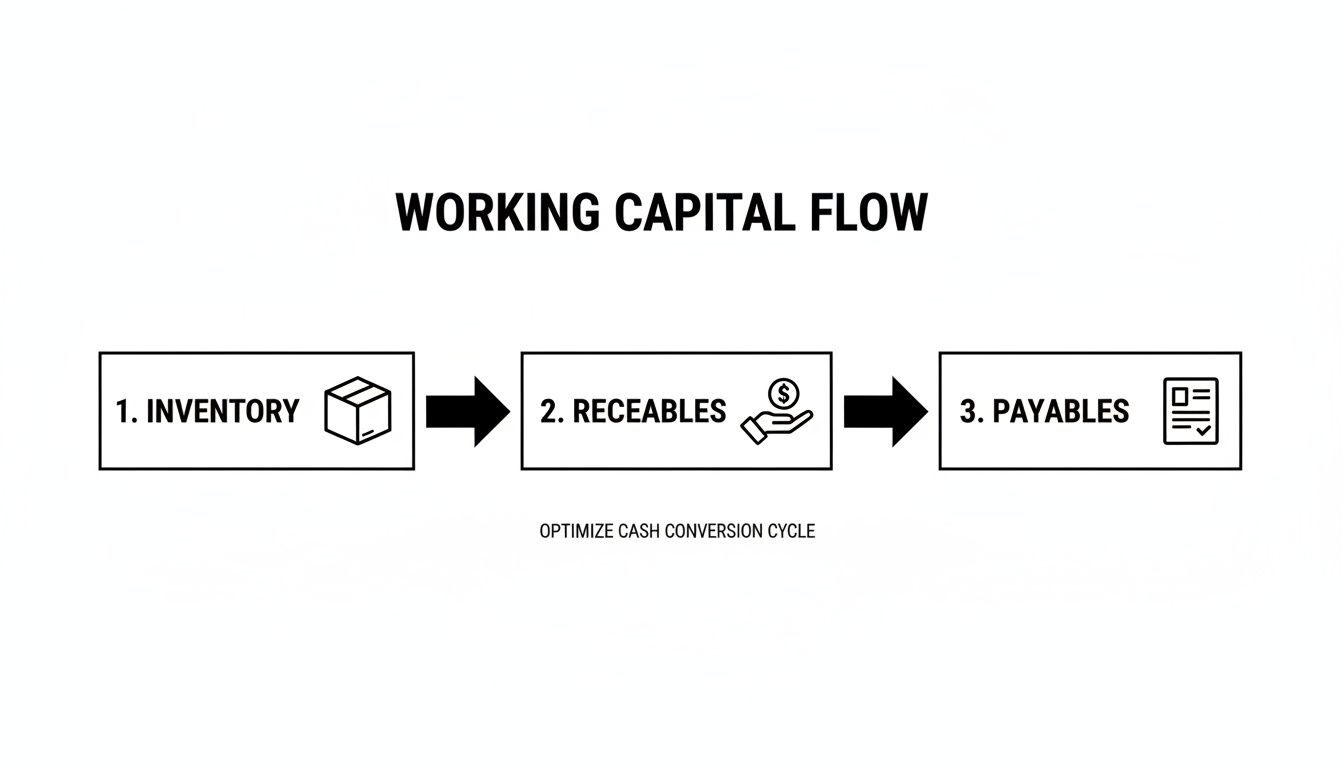

When we talk about working capital, it’s easy to get lost in spreadsheets and financial jargon. But really, it all boils down to seeing your business’s cash not as a fixed number in a bank account, but as water flowing through your operations.

This cash is constantly moving between three key areas. Getting a handle on this flow is the difference between struggling to keep the lights on and having the fuel you need to scale. Let's look at exactly where your cash gets tied up.

For any brand selling physical products, inventory is almost always the biggest cash hog. Every single item sitting in your warehouse or at a 3PL is basically a stack of cash you can’t spend. It’s money you’ve already paid that does nothing for you until a customer clicks "buy."

Finding the right inventory level is a constant tightrope walk.

The smartest sellers don't just see boxes on a shelf; they see a pool of capital. Your job is to keep that pool just deep enough to swim in, without it overflowing.

In the world of e-commerce, Accounts Receivable (AR) isn't about chasing down late customer payments. It’s about the frustrating, built-in delay between when a customer pays you and when you can actually access that money.

When someone buys your product on Amazon, through Shopify Payments, or on any other marketplace, that cash takes a little detour. It sits with the platform for days or sometimes even weeks before it lands in your bank account.

Imagine you have a great day and sell $10,000 worth of product. If your payment processor works on a 14-day payout cycle, that $10,000 is your money, but it's stuck. You've essentially given them a short-term, interest-free loan.

For a brand that’s growing fast, this "payout lag" can cause a major cash crunch. You need to pay your supplier for a new PO today, but the cash from all your recent sales won't show up for another two weeks. This timing mismatch is a classic working capital trap that catches a lot of sellers off guard.

Accounts Payable (AP) is simply the money you owe to others, mainly your suppliers. It’s easy to think of this as just another bill to pay as fast as possible, but savvy founders see it differently. They see it as a powerful cash flow tool.

Think of your payment terms as a form of short-term, interest-free financing. Negotiating better terms is one of the single best moves you can make.

The longer you can hold onto your cash before paying your bills, the more work it can do for you. You can use it to fund operations, run more ads, or place another inventory order, all before that supplier invoice is due. This is what smart working capital management looks like in practice.

Unfortunately, it’s not always a level playing field. Recent research shows that the time it takes for UK businesses to turn their operations into cash has shot up by 48.0% since 2017. For smaller e-commerce brands, it's even tougher—their working capital needs have gotten worse by 13.5% as bigger companies use their muscle to hoard cash. You can read the full research about e-commerce supply chains to get the bigger picture on these trends.

Knowing the three pillars of working capital—inventory, receivables, and payables—is a great start. But the real magic happens when you start measuring them. To truly get a handle on what is working capital management is, you need to track the speed at which cash moves through your business.

This is where the Cash Conversion Cycle (CCC) comes in.

The CCC is one of the most powerful numbers you can track as an e-commerce business owner. It tells you, in days, exactly how long it takes for the cash you spent on inventory to travel all the way back into your bank account after a customer pays.

A shorter CCC is always better. It means your cash isn't just sitting around—it's actively working for you, fueling growth.

This single metric gives you a high-level snapshot of your operational health. It's calculated by combining three other key performance indicators (KPIs) that line up perfectly with our three pillars.

This diagram shows you exactly what that flow looks like—how you juggle inventory and receivables while managing what you owe to suppliers.

This whole process boils down to one core challenge: you have to spend cash on inventory and operations before you ever see a dime from your customers. Your goal is to shrink that time gap as much as humanly possible.

First up is Days Inventory Outstanding (DIO), which you'll often hear called inventory days. This KPI measures the average number of days it takes you to sell through your entire stock. It answers a simple but crucial question: "How long is my cash tied up in products just sitting on a shelf?"

A high DIO is a major red flag. It means your inventory is collecting dust, piling up storage fees, and getting closer to becoming obsolete. A low DIO, on the other hand, tells you that you're turning products over quickly.

The formula is straightforward:

DIO = (Average Inventory / Cost of Goods Sold) x 365 Days

Let's say your average inventory is $50,000 and your annual COGS is $200,000. Your DIO would be 91 days. That means it takes you roughly three months to convert your inventory into sales.

Next, we have Days Sales Outstanding (DSO). This metric tracks how long it takes to actually collect your cash after you've made a sale. For anyone selling online, this is all about the payout lag from platforms like Amazon, Shopify Payments, and other payment gateways.

The higher your DSO, the longer your hard-earned revenue is stuck in someone else's system instead of your own bank account. A high DSO can cause some serious cash flow headaches, forcing you to fund daily operations out-of-pocket while you wait to get paid.

The formula for DSO is:

DSO = (Average Accounts Receivable / Total Credit Sales) x 365 Days

For instance, if you have an average of $20,000 in receivables and bring in $500,000 in annual sales, your DSO is 14.6 days. That's pretty standard for many platforms, but chipping away at that number can make a massive difference to your cash flow. Our guide on what is days sales outstanding dives into more advanced strategies for tackling this.

Finally, there's Days Payable Outstanding (DPO). This metric measures the average time it takes you to pay your own bills—like inventory from suppliers.

Here’s the twist: unlike DIO and DSO, a higher DPO is generally a good thing. It means you're holding onto your cash longer, essentially using your supplier's credit as a form of interest-free financing.

A low DPO means you’re paying your bills too fast, giving up precious cash you could be using elsewhere. Simply negotiating longer payment terms (like moving from Net 30 to Net 60) is one of the quickest ways to improve your working capital position.

The formula looks like this:

DPO = (Average Accounts Payable / Cost of Goods Sold) x 365 Days

If you have an average of $30,000 in accounts payable against a $200,000 COGS, your DPO is 54.75 days. In this scenario, you're effectively using almost two months of your suppliers' money to finance your business.

To really master your cash cycle, you need to stay on top of the relevant Financial KPIs. These numbers aren't just for accountants; they give you the insights needed to make smarter decisions and steer your business toward a much healthier financial future.

Knowing your numbers is one thing. Actually improving them is where the real magic happens. Think of effective working capital management as having a control panel for your business's cash flow—it’s all about knowing which levers to pull, and when, to free up the money that’s stuck inside your operations.

Let's get into the practical tactics. We'll break them down by the three pillars of working capital, so you can start shortening your cash conversion cycle and pouring that fuel back into your growth.

For almost every ecommerce seller, inventory is the biggest cash sink. It's simple: every dollar you spend on a product that just sits on a shelf is a dollar you can't use for marketing, new product launches, or just paying the bills. The goal is to walk that fine line—holding just enough stock to meet demand without tying up a fortune in capital.

Implement Smart Demand Forecasting

Stop guessing or just re-ordering what sold well last year. It’s time to use real data to predict future sales. Dig into seasonality, watch for market trends, and factor in how your marketing campaigns will affect demand. This allows you to make much sharper purchasing decisions.

This isn't just a "nice-to-have" practice; it's a financial game-changer. One analysis of online brands showed that when you align your inventory buys with genuine sales forecasts, you can slash the cash conversion cycle by 20-30%. For founders, that’s cash unlocked for scaling—without taking on expensive debt. You can learn more about this working capital insight and see just how critical timing can be.

Rationalize Your SKUs

Not every product in your catalog is a winner. You need to regularly run an ABC analysis to figure out what’s what:

Get ruthless with your C-Items. Liquidate them, discontinue them, do what you have to do. A flash sale might feel like a hit to your margins on those specific products, but the cash injection it gives your business is almost always worth more.

In the world of ecommerce, "receivables" isn't about chasing down unpaid invoices. It's all about closing the "payout lag" from marketplaces like Amazon and your payment processors. Every day you can shave off your Days Sales Outstanding (DSO) puts cash back into your bank account that much faster.

Negotiate Payout Schedules

It’s tough to do with a giant like Amazon, but some smaller marketplaces or payment processors might be willing to talk, especially once you've got some solid sales volume. Don't be afraid to ask if you can move from a 14-day payout cycle to a 7-day, or even a 3-day schedule.

Consider Invoice or Receivable Financing

There are services out there that will advance you the cash tied up in your marketplace payouts, usually for a small fee. This isn’t a loan—it’s a way to get your hands on your own money sooner. It's a fantastic tool to fund a big inventory order right after a huge sales weekend like Black Friday, bridging the cash gap until your revenue finally lands. Mastering effective small business cash flow management is a must, and tools like these can be a vital part of your strategy.

This is one of the most powerful, and most overlooked, tools you have. Your Accounts Payable is essentially a source of short-term, interest-free financing. Every extra day your suppliers give you to pay them is another day you can use that cash to fund your operations. The key is to increase your Days Payable Outstanding (DPO) without burning bridges with your suppliers.

Negotiate Longer Payment Terms

This is one of the single most effective moves you can make to improve your working capital. If you’re currently on Net 30 terms, try asking for Net 45 or Net 60. Don’t just ask for it—frame it as a way to support larger, more consistent orders from them down the line.

Utilize Trade Credit and Supply Chain Financing

Some of your bigger suppliers might offer formal trade credit programs, so be sure to ask. Another option is supply chain financing, where a third-party funder pays your supplier early (often at a small discount) while you get to keep your longer payment terms. It’s a win-win: your supplier gets paid fast, and you get to hold onto your cash. Our guide on ways to improve cash flow has more great ideas on this front.

Even if your operations are running like a well-oiled machine, fast-growing e-commerce brands eventually hit a wall. You'll need a cash injection at some point. Maybe it's to fund a massive Q4 inventory order or to bridge a gap while you expand into a new market. A huge part of working capital management is knowing when—and how—to get that outside funding.

The good news? You don't have to go hat-in-hand to a traditional bank anymore. There’s a whole new world of financing built just for the fast-paced nature of online retail. Picking the right one can launch your growth, but the wrong one can trap you in bad terms or force you to give up a chunk of your company.

Let’s be honest, traditional banks just don’t get e-commerce. They get hung up on things like physical storefronts and decades of operating history, totally missing the value of a killer brand with soaring online sales. Modern funders are different; they plug right into your sales platforms and actually understand your business model.

This new wave of financing is faster, way more flexible, and often doesn't require you to give up equity. But to make a smart choice, you really need to get the lay of the land. Our article comparing equity financing vs. debt financing is a great place to start for that essential background.

Trying to sort through all the options can feel overwhelming, but it boils down to what you need the money for. We’ve put together a quick comparison to help you see how the top solutions stack up for a growing brand.

As you weigh your options, think about the total cost and how flexible the repayments are. Revenue-based financing, for instance, is a game-changer because your payments move with your sales. If you have a slow month, you pay back less, which is a huge relief for your cash flow.

The rise of private credit funds, which have grown to over €2 trillion in assets, has fueled many of these alternative financing solutions. These funds are stepping in where banks have pulled back, offering faster, more flexible deals for growing businesses.

Choosing the right funding partner is just as critical as choosing the right type of financing. You want someone who lives and breathes e-commerce and can be more of a strategic partner than just a lender. The end goal is to find capital that actually works for you, fueling your next big move without becoming a dead weight.

Alright, you've crunched the numbers and have a good grasp of the metrics. Now what? Turning all that data into actual, smart decisions is where the magic really happens.

This isn't about buying some complicated, expensive software. An effective working capital system is simply a repeatable process—a routine—that gives you a crystal-clear picture of your cash flow. It’s about building a financial command center that helps you make better calls, day in and day out.

The bedrock of any solid system is simple consistency. You need to create a habit of stepping back from the daily grind to look at the bigger financial picture. Think of it as a monthly financial check-up.

You don't need anything fancy. A basic spreadsheet is the perfect place to start. Here's a simple checklist to run through each month:

This simple ritual turns abstract numbers into a dashboard you can actually use, helping you spot trouble long before it becomes a full-blown crisis.

You don't need an expensive enterprise-level system to get started. Your toolkit can, and should, grow with your business.

The tool itself isn’t what matters. It's the discipline to actually use it. A simple spreadsheet you update every month is infinitely more powerful than a sophisticated dashboard you ignore. It’s all about building that habit of financial oversight.

A truly great system doesn't just track the past; it prepares you for the future. The best way to build your decision-making muscle is to run fire drills for common e-commerce curveballs.

Scenario 1: A top supplier suddenly shortens your payment terms from Net 60 to Net 30.

Scenario 2: One of your products unexpectedly goes viral, and sales triple overnight.

Once you start digging into working capital, a lot of questions pop up. It’s normal. Founders are always trying to figure out if they’re on the right track or if there’s a massive problem hiding just under the surface.

Let’s tackle some of the most common questions we see and give you answers you can actually use.

Everyone wants a magic number, but it doesn't really exist. The textbook answer is to aim for a ratio between 1.2 and 2.0, and that’s a decent starting point.

But context is everything. A brand-new DTC company might run lean with a lower ratio, while a reseller sitting on a mountain of inventory needs to be on the higher end of that 1.2 to 2.0 range to stay safe.

The real key? Track your own ratio over time. A number that’s consistently low or, worse, negative, is your canary in the coal mine—a sign that a cash flow crisis is brewing.

Hands down, the biggest mistake is buying too much inventory. Especially slow-moving products. That’s just cash, sitting in a box, collecting dust instead of funding your marketing or next big product launch.

Another huge one is not pushing back on supplier payment terms. When you pay your suppliers long before your customers pay you, you're basically giving them a free loan and creating your own cash crunch. Too many founders just accept the terms they're given, and it bleeds them dry.

They just aren't looking at their Cash Conversion Cycle—until it's too late.

The most successful founders view working capital not as an accounting task, but as a strategic weapon. They are obsessed with shortening the time it takes to turn inventory back into cash, because they know that cash is the fuel for growth.

You don't need a huge bankroll to make a difference. Start with the levers you can pull right now, for free.

First, get ruthless with your inventory. Find your slow-movers and liquidate them. Yes, even if it’s at a discount. Getting that cash back in your hands today is almost always the right move.

Next, pick up the phone and talk to your suppliers. Ask for better terms. Moving from Net 30 to Net 45 or even Net 60 is a game-changer. Finally, look at your sales channels. Which ones pay you the fastest? Push more volume through them. These moves cost you nothing but can seriously improve your cash position.

At Million Dollar Sellers, top e-commerce founders share the exact strategies they use to optimize cash flow and scale past 7, 8, and 9 figures. If you're ready to learn from the best in the business, find out if you qualify for our exclusive community. Learn more about MDS.

Join the Ecom Entrepreneur Community for Vetted 7-9 Figure Ecommerce Founders

Learn MoreYou may also like:

Learn more about our special events!

Check Events